Key Insights

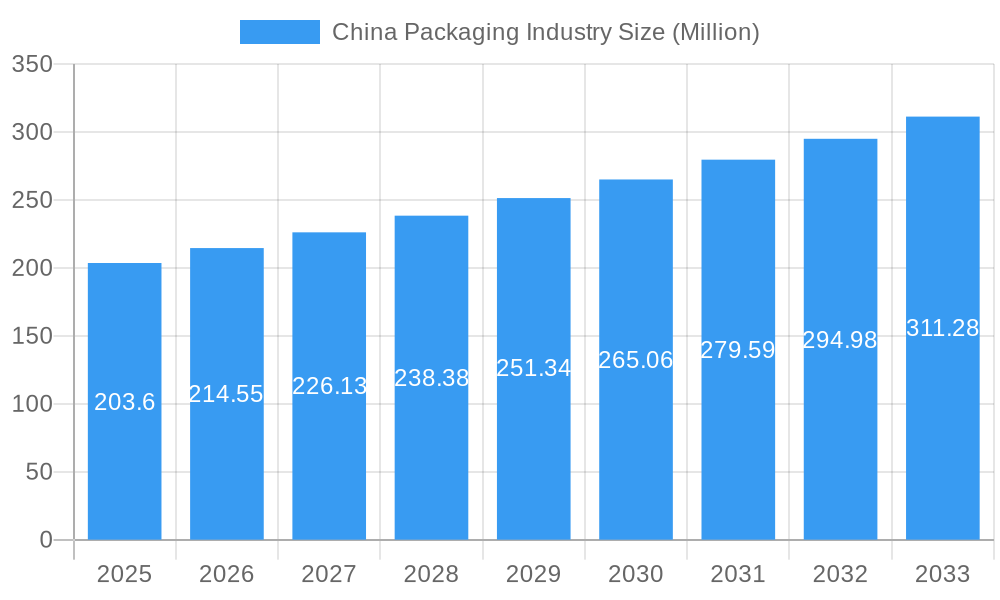

The China packaging industry, valued at $203.60 million in 2025, is projected to experience robust growth, driven by a burgeoning e-commerce sector, rising consumer spending, and increasing demand for convenient and sustainable packaging solutions across diverse end-user industries. The 5.22% CAGR from 2019 to 2033 indicates a significant expansion, particularly within the food and beverage, healthcare, and beauty and personal care sectors. Growth is fueled by the adoption of innovative packaging materials like biodegradable plastics and advanced barrier films, enhancing product preservation and shelf life. This trend aligns with increasing consumer awareness of environmental sustainability and government regulations promoting eco-friendly packaging. While challenges remain, including fluctuating raw material prices and stringent regulatory compliance requirements, the overall outlook for the China packaging market remains positive. The market is segmented by packaging material (plastic, paper, glass, foam, metal), packaging layers (primary, secondary, tertiary), and end-user industries. Key players like Amcor PLC, Mondi PLC, and Tetra Pak International SA are strategically positioned to benefit from this growth trajectory through investments in advanced technologies and expansion of their product portfolios. The competitive landscape is further shaped by regional players, particularly those focused on catering to the growing domestic demand.

China Packaging Industry Market Size (In Million)

The projected growth trajectory is influenced by several factors, including sustained economic growth in China, urbanization, and evolving consumer preferences. The shift towards online retail has significantly increased the demand for e-commerce-ready packaging, while the growing middle class is driving demand for premium packaging in sectors like cosmetics and food and beverages. However, challenges like stringent environmental regulations and the need to adopt sustainable practices are shaping the industry's future. Companies are increasingly focusing on sustainable packaging materials and improving their supply chain efficiency to meet growing demand while adhering to environmental compliance. The competitive landscape is dynamic, with both multinational corporations and local manufacturers competing for market share. Innovation in packaging design and materials will continue to be a key factor in determining market success in the years to come. The forecast period of 2025-2033 presents significant opportunities for growth and expansion within the China packaging industry.

China Packaging Industry Company Market Share

China Packaging Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the China packaging industry, offering invaluable insights for stakeholders across the value chain. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report meticulously examines market dynamics, key segments, leading players, and future opportunities. The report uses Million for all values.

China Packaging Industry Market Concentration & Dynamics

The China packaging industry is characterized by a dynamic interplay of established players and emerging businesses. Market concentration is moderate, with several large multinational corporations and numerous smaller, regional players competing for market share. Key metrics, such as market share, reveal a fragmented landscape, although some dominant players control significant portions of specific segments. For instance, the market share of Amcor PLC and Mondi PLC in the paper packaging segment is estimated at xx Million and xx Million respectively in 2025. The industry's innovation ecosystem is vibrant, driven by ongoing research and development in sustainable and technologically advanced packaging solutions. The regulatory framework is constantly evolving, focusing on environmental protection and food safety. Substitute products, such as reusable containers and bulk packaging, are gaining traction, presenting challenges and opportunities for traditional players. End-user trends are shifting towards greater convenience, sustainability, and e-commerce-friendly packaging. Mergers and acquisitions (M&A) activity is substantial, with an estimated xx M&A deals in the period 2019–2024, showcasing industry consolidation and strategic expansion.

- Market Share: Amcor PLC (xx Million), Mondi PLC (xx Million), other players (xx Million) in 2025.

- M&A Activity: xx deals in 2019-2024.

- Regulatory Focus: Environmental sustainability and food safety.

- Substitute Products: Reusable containers and bulk packaging gaining popularity.

China Packaging Industry Industry Insights & Trends

The China packaging market is experiencing robust growth, driven by a burgeoning consumer class, rapid urbanization, and a rise in e-commerce. The market size in 2025 is estimated at xx Million, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Key growth drivers include increasing demand across various end-user industries, technological advancements in packaging materials and technologies, and a growing preference for customized and sustainable packaging. Technological disruptions, particularly in automation and digital printing, are reshaping manufacturing processes and improving efficiency. Evolving consumer behaviors, including increased focus on convenience, product safety, and environmental consciousness, are influencing packaging choices and design preferences. A notable shift is the increasing adoption of e-commerce packaging solutions, optimized for logistics and consumer experience. The market is witnessing increased investments in sustainable and eco-friendly packaging materials to meet environmental regulations and consumer demand.

Key Markets & Segments Leading China Packaging Industry

The China packaging industry is a dynamic and multifaceted landscape, characterized by distinct segments with varying growth potentials. Thorough market analysis reveals that plastic and paper-based packaging materials are the dominant forces, underpinning a vast array of applications across the nation. While regional nuances exist, these material types consistently lead in market share.

-

By Packaging Material:

- Plastic Packaging: Continues to lead due to its exceptional versatility, cost-effectiveness, and adaptability across numerous product categories.

- Paper Packaging: Holds a substantial and growing share, significantly propelled by increasing consumer and regulatory demand for sustainable and eco-friendly solutions, particularly in the food and beverage sectors.

- Metal Packaging: Demonstrates robust growth, especially within the premium food and beverage segment, where its protective qualities and aesthetic appeal are highly valued.

- Glass Packaging: Maintains a stable market presence, with notable expansion in premium and specialty product categories that benefit from its perceived quality and inertness.

- Foam Packaging: Carves out essential niches, primarily for protective applications and cushioning sensitive goods during transit and handling.

-

By Layers of Packaging:

- Primary Packaging: Commands the largest market share, directly enclosing and protecting the product, hence its consistent high demand.

- Secondary Packaging: Follows primary packaging, offering additional protection, branding, or grouping of products.

- Tertiary Packaging: Used for bulk handling, shipping, and warehousing, facilitating efficient logistics.

-

By End-user Industry:

- Food & Beverage: Remains the paramount end-user, driven by sheer volume and variety of products requiring packaging.

- Healthcare & Pharmaceutical: A rapidly growing segment, demanding high standards of safety, sterility, and traceability.

- The burgeoning e-commerce sector and a societal shift towards convenience-oriented consumption are significantly boosting the need for sophisticated primary and secondary packaging solutions across these industries, emphasizing product protection, shelf appeal, and user experience.

Key Market Drivers:

- Accelerated economic expansion and pervasive urbanization.

- The exponential growth of the e-commerce landscape and online retail.

- A burgeoning middle class with increasing disposable incomes and a desire for higher-quality goods.

- Elevated consumer demand for convenient, on-the-go products and premium offerings.

- The implementation of stringent government regulations pertaining to food safety, product integrity, and environmental sustainability.

China Packaging Industry Product Developments

The China packaging industry is currently experiencing a period of intense innovation, with a pronounced focus on sustainability and advanced functionality. Manufacturers are making substantial investments in the research and development of biodegradable, compostable, and recyclable packaging materials to mitigate environmental impact and meet growing eco-consciousness. Concurrently, the integration of smart packaging technologies, such as RFID tags for enhanced supply chain traceability, QR codes for consumer engagement, and tamper-evident features for security, is rapidly increasing. These advancements not only provide companies with a significant competitive advantage but also directly address the evolving demands of both consumers and regulatory bodies. Furthermore, the adoption of active and intelligent packaging solutions is on the rise, aiming to improve food preservation, extend shelf life, and monitor product condition throughout the supply chain.

Challenges in the China Packaging Industry Market

The China packaging industry faces several significant challenges, including stringent environmental regulations, which may increase production costs. Supply chain disruptions, exacerbated by geopolitical factors and raw material price volatility, pose another significant hurdle. Intense competition from both domestic and international players adds pressure on profit margins. These factors collectively impede industry growth and necessitate strategic adaptation. In 2024, estimated losses due to supply chain issues were approximately xx Million.

Forces Driving China Packaging Industry Growth

A confluence of powerful forces is propelling the growth of China's packaging industry. Significant advancements in materials science and manufacturing technologies are leading to greater efficiency, enhanced product quality, and the development of novel packaging formats. Government initiatives aimed at supporting domestic manufacturing, promoting industrial upgrades, and investing in logistics infrastructure are creating a favorable ecosystem for expansion. The continuous rise in consumer spending power and evolving lifestyle preferences, characterized by a demand for diverse, convenient, and aesthetically pleasing products, directly translates into a higher need for sophisticated packaging solutions. Moreover, government policies actively championing sustainability and circular economy principles are reshaping market trends, driving the adoption of eco-friendly materials and responsible packaging practices.

Challenges in the China Packaging Industry Market

Long-term growth in the China packaging industry is hinged on addressing several crucial challenges. These include overcoming the issues surrounding supply chain resilience and diversifying sourcing strategies. Investing heavily in research and development to create innovative, sustainable packaging solutions is paramount. Strategic partnerships and collaborations can unlock new market opportunities and drive efficiency improvements. Expanding into new markets and geographical areas will mitigate risks associated with over-reliance on a single market.

Emerging Opportunities in China Packaging Industry

Several exciting opportunities are emerging within the China packaging market. The rapid growth of e-commerce opens avenues for specialized packaging solutions tailored to online retail. Increasing demand for sustainable and eco-friendly options presents immense opportunities for businesses offering biodegradable and recyclable materials. The increasing adoption of smart packaging technologies, such as active and intelligent packaging, offers scope for innovation and enhanced product value.

Leading Players in the China Packaging Industry Sector

- Daklapack Group

- Transpak Inc

- Sealed Air Corporation

- Jiangyin Aluminum Foil Packaging East Asia Co Ltd

- Plastipak Holdings Inc

- Amcor PLC

- Mondi PLC

- Wipak Group

- Guangzhou Yifeng Printing & Packaging Co Ltd

- Tetra Pak International SA

Key Milestones in China Packaging Industry Industry

August 2022: Nippon Paint China and BASF jointly introduced eco-friendly industrial packaging for Nippon Paint's dry-mixed mortar products using BASF's water-based acrylic dispersion. This launch marks a significant step towards sustainable packaging solutions within the industrial sector in China.

March 2022: Datwyler's full acquisition of Yantai Xinhui Packing, a Chinese pharmaceutical packaging manufacturer, strengthens Datwyler's position in the Chinese market and enhances its product portfolio in the healthcare sector.

Strategic Outlook for China Packaging Industry Market

The future trajectory of the China packaging industry is exceptionally promising, characterized by sustained growth driven by technological innovation, evolving consumer expectations, and proactive government policies. The market's evolution will be significantly shaped by the pervasive adoption of sustainable packaging solutions and the seamless integration of smart technologies, which will redefine product protection, traceability, and consumer interaction. To maintain a competitive advantage, companies must prioritize strategic investments in cutting-edge research and development, cultivate robust partnerships, and foster collaborative ventures across the value chain. The market presents immense opportunities for groundbreaking innovation and expansion, particularly within the rapidly growing segments of e-commerce fulfillment and premium consumer goods.

China Packaging Industry Segmentation

-

1. Packaging Material

- 1.1. Plastic

- 1.2. Paper

- 1.3. Glass

- 1.4. Metal

- 1.5. Other Packaging Material

-

2. Types of Packaging

- 2.1. Primary Packaging

- 2.2. Secondary Packaging

- 2.3. Tertiary Packaging

-

3. End-user Industry

- 3.1. Food and Beverage

- 3.2. Healthcare and Pharmaceutical

- 3.3. Beauty and Personal Care

- 3.4. Industrial

- 3.5. Other End-user Industries

China Packaging Industry Segmentation By Geography

- 1. China

China Packaging Industry Regional Market Share

Geographic Coverage of China Packaging Industry

China Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 5.1.1. Plastic

- 5.1.2. Paper

- 5.1.3. Glass

- 5.1.4. Metal

- 5.1.5. Other Packaging Material

- 5.2. Market Analysis, Insights and Forecast - by Types of Packaging

- 5.2.1. Primary Packaging

- 5.2.2. Secondary Packaging

- 5.2.3. Tertiary Packaging

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverage

- 5.3.2. Healthcare and Pharmaceutical

- 5.3.3. Beauty and Personal Care

- 5.3.4. Industrial

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6. China Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6.1.1. Plastic

- 6.1.2. Paper

- 6.1.3. Glass

- 6.1.4. Metal

- 6.1.5. Other Packaging Material

- 6.2. Market Analysis, Insights and Forecast - by Types of Packaging

- 6.2.1. Primary Packaging

- 6.2.2. Secondary Packaging

- 6.2.3. Tertiary Packaging

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverage

- 6.3.2. Healthcare and Pharmaceutical

- 6.3.3. Beauty and Personal Care

- 6.3.4. Industrial

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Daklapack Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Transpak Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sealed Air Corporation*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Jiangyin Aluminum Foil Packaging East Asia Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Plastipak Holdings Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Amcor PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mondi PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wipak Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Guangzhou Yifeng Printing & Packaging Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tetra Pak International SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Daklapack Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: China Packaging Industry Revenue Million Forecast, by Packaging Material 2020 & 2033

- Table 2: China Packaging Industry Revenue Million Forecast, by Types of Packaging 2020 & 2033

- Table 3: China Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: China Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: China Packaging Industry Revenue Million Forecast, by Packaging Material 2020 & 2033

- Table 6: China Packaging Industry Revenue Million Forecast, by Types of Packaging 2020 & 2033

- Table 7: China Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: China Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Packaging Industry?

The projected CAGR is approximately 5.22%.

2. Which companies are prominent players in the China Packaging Industry?

Key companies in the market include Daklapack Group, Transpak Inc, Sealed Air Corporation*List Not Exhaustive, Jiangyin Aluminum Foil Packaging East Asia Co Ltd, Plastipak Holdings Inc, Amcor PLC, Mondi PLC, Wipak Group, Guangzhou Yifeng Printing & Packaging Co Ltd, Tetra Pak International SA.

3. What are the main segments of the China Packaging Industry?

The market segments include Packaging Material, Types of Packaging, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 203.60 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-commerce Giants; Increasing Demand for Longer Shelf Life of Packaged Goods.

6. What are the notable trends driving market growth?

Plastic Packaging is Expected to Witness a Slow Growth Owing to Ban on Plastics.

7. Are there any restraints impacting market growth?

Strict Rules and Regulations in the Packaging Industry; Environmental Concerns Restricting the Market Growth.

8. Can you provide examples of recent developments in the market?

August 2022: Nippon Paint China, a prominent coatings producer, and BASF jointly introduced eco-friendly industrial packaging, which Nippon Paint's dry-mixed mortar series products have since embraced. The innovative packaging material for Nippon Paint's construction dry mortar products is commercialized, using water-based acrylic dispersion Joncryl High-Performance Barrier (HPB) from BASF as the barrier material. China will be the first country where BASF's water-based barrier coatings are employed in industrial packaging.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Packaging Industry?

To stay informed about further developments, trends, and reports in the China Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence