Key Insights

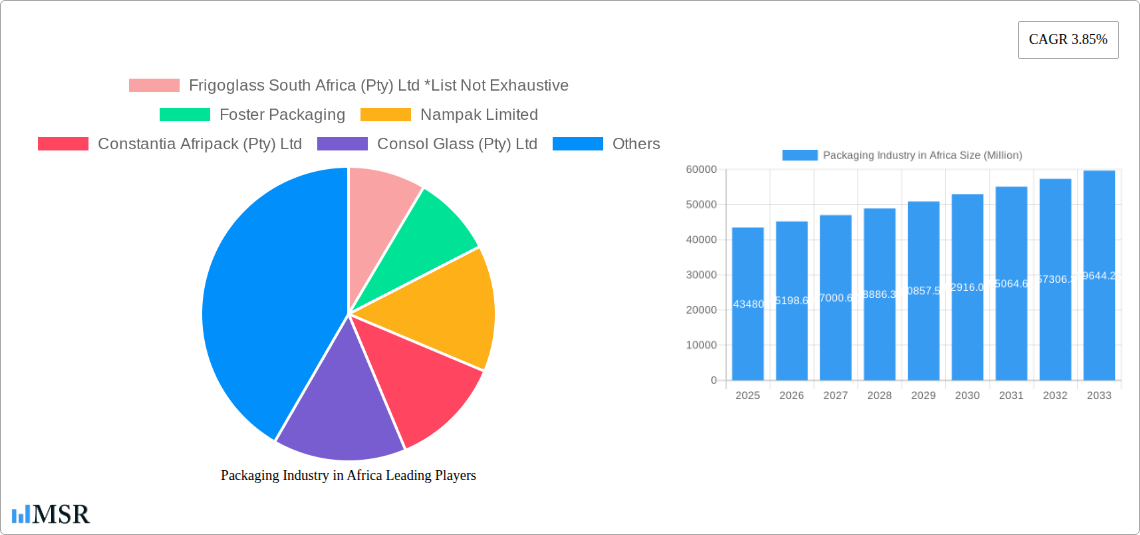

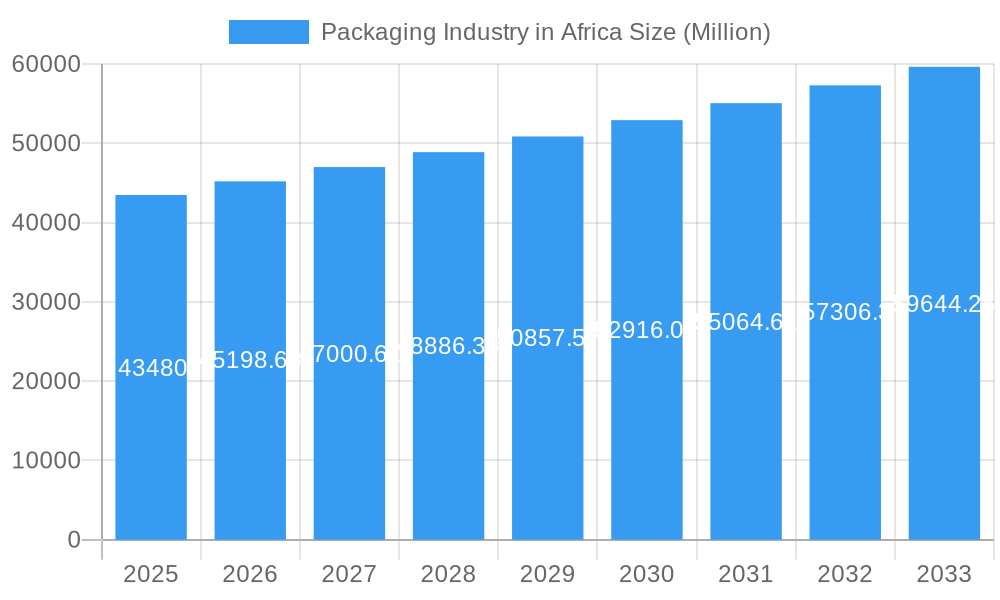

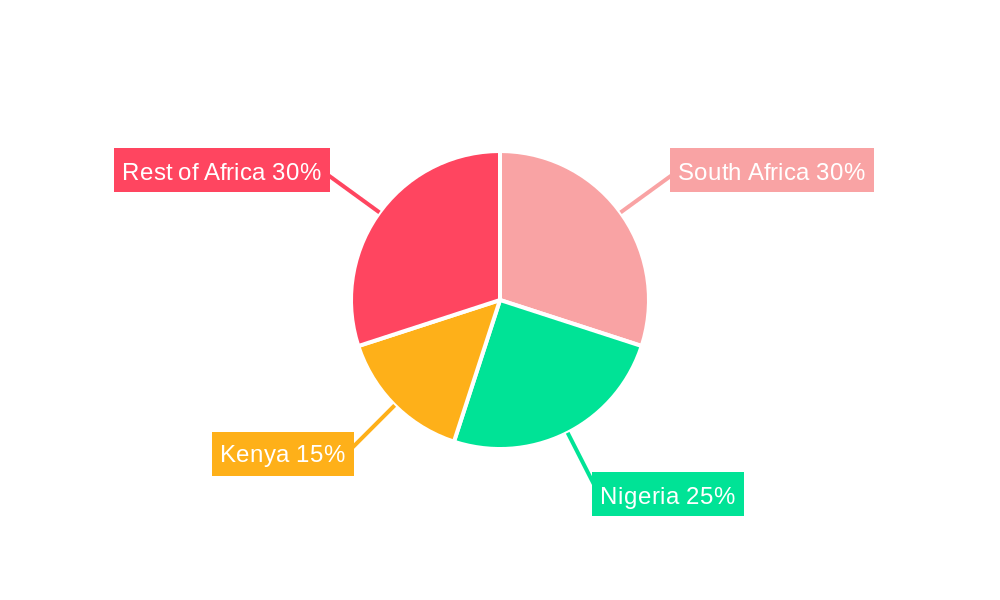

The African packaging market, valued at $43.48 billion in 2025, is projected to experience robust growth, exhibiting a compound annual growth rate (CAGR) of 3.85% from 2025 to 2033. This expansion is fueled by several key drivers. A burgeoning population and rising disposable incomes are stimulating increased consumption of packaged goods across various sectors, including food, beverages, pharmaceuticals, and personal care. The growth of organized retail and e-commerce further accelerates demand for efficient and attractive packaging solutions. Furthermore, the increasing adoption of sustainable packaging materials, driven by growing environmental awareness and stringent regulations, presents significant opportunities for eco-friendly packaging solutions. Specific growth areas include flexible packaging for food and beverages, owing to its cost-effectiveness and convenience, and the increasing demand for customized packaging solutions reflecting brand identities. Challenges, however, include inadequate infrastructure in some regions, hindering efficient logistics and distribution of packaged goods. Additionally, fluctuating raw material prices and intense competition among packaging companies pose potential restraints on market growth. South Africa, Nigeria, and Kenya represent the largest national markets, though significant growth potential exists in other rapidly developing African nations.

Packaging Industry in Africa Market Size (In Billion)

The market segmentation reveals diverse opportunities. Paper and paperboard remain dominant materials, driven by their affordability and versatility, especially for corrugated boxes catering to the food and beverage sectors. Plastic packaging, despite environmental concerns, retains significant market share due to its durability and cost-effectiveness in applications like bottles. Metal cans, particularly for beverages, and glass bottles for premium products maintain a niche. The beverage industry commands a substantial share, with food and pharmaceuticals showing strong growth potential, creating diverse opportunities for specialized packaging solutions. Companies like Nampak Limited, Consol Glass, and Mondi Group are key players, leveraging their established presence and expanding their product offerings to cater to evolving consumer preferences and environmental regulations. Future growth will be significantly impacted by government policies promoting sustainable packaging practices and investments in improving logistics infrastructure across the continent.

Packaging Industry in Africa Company Market Share

Packaging Industry in Africa: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the African packaging industry, covering market dynamics, key trends, leading players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry stakeholders, investors, and businesses seeking to understand and capitalize on opportunities within this rapidly evolving market. The report is based on extensive research and incorporates data from 2019-2024, providing a comprehensive historical perspective. The market is valued at xx Million USD in 2025.

Packaging Industry in Africa Market Concentration & Dynamics

The African packaging market exhibits a moderately concentrated landscape, with several multinational corporations and large regional players dominating specific segments. Market share is largely influenced by factors such as production capacity, distribution networks, and brand recognition. Nampak Limited and Mondi Group, for example, hold significant market shares across multiple product categories. Innovation is driven by both established players and emerging local businesses responding to unique African market needs. Regulatory frameworks vary across countries, impacting material choices and sustainability initiatives. Substitute products, such as reusable containers, present a growing challenge, particularly as environmental awareness increases. End-user trends favor convenience, sustainability, and e-commerce-friendly packaging solutions. M&A activities, as exemplified by Ardagh Group's acquisition of Consol Holdings in 2022 (USD 1 Billion deal), demonstrate significant investment and consolidation within the industry.

- Market Concentration: Moderately concentrated, with several dominant players.

- Innovation Ecosystem: A mix of established players and agile startups.

- Regulatory Frameworks: Vary across African nations, influencing material selection.

- Substitute Products: Growing influence of reusable and sustainable alternatives.

- End-User Trends: Demand for convenience, sustainability, and e-commerce-friendly packaging.

- M&A Activity: Significant consolidation with major deals like the Ardagh/Consol acquisition in 2022 (USD 1 Billion).

Packaging Industry in Africa Industry Insights & Trends

The African packaging market is experiencing robust growth, driven by factors such as rising disposable incomes, expanding consumer base, and urbanization. The market size is estimated to reach xx Million USD by 2025 with a CAGR of xx% during the forecast period. Technological advancements in materials science, automation, and printing technologies are transforming the industry. E-commerce growth is fueling demand for protective and efficient packaging solutions. Consumer preferences are shifting towards eco-friendly and sustainable options, pushing companies to adopt recycled materials and improve packaging recyclability. The increasing adoption of flexible packaging is also noted. Furthermore, changing consumer preferences and tastes influence packaging designs and functionalities.

Key Markets & Segments Leading Packaging Industry in Africa

South Africa remains a dominant market, followed by Nigeria and Egypt. However, growth is strong across the continent, particularly in rapidly developing economies. Within segments:

- By Material: Plastic packaging currently holds the largest market share due to cost-effectiveness and versatility, followed by paper and paperboard. Glass and metal packaging hold niche markets, especially within the beverage and food sectors.

- By Product Type: Plastic bottles and corrugated boxes are the most prevalent product types, reflecting the high demand in the beverage and food industries, respectively.

- By End-user Industry: The food and beverage sectors are the biggest consumers, accounting for xx Million USD in 2025, driven by increased demand for packaged food and beverages. The pharmaceutical and household and personal care sectors also show promising growth.

- By Country: South Africa, Egypt, and Nigeria are the leading national markets, representing a significant portion of the total market value. Growth in Kenya and other East African countries also shows significant potential.

Growth Drivers:

- Strong economic growth in several African countries.

- Expanding middle class with increased disposable income.

- Urbanization and changing lifestyles.

- Rising demand for packaged food and beverages.

- Growth of the e-commerce sector.

Packaging Industry in Africa Product Developments

Recent innovations include lightweight, sustainable materials, improved barrier properties for extended shelf life, and increased customization options using advanced printing technologies. These developments aim to enhance product protection, improve sustainability, and cater to specific brand requirements. The focus on reducing environmental impact is driving the development of recyclable and compostable packaging solutions.

Challenges in the Packaging Industry in Africa Market

Significant challenges include inconsistent infrastructure, fluctuating raw material costs, and access to advanced technologies. Regulatory inconsistencies across different countries also pose hurdles for standardization and compliance. Furthermore, counterfeit packaging remains a challenge impacting brand protection and consumer trust. The lack of organized waste management systems hinders recycling efforts.

Forces Driving Packaging Industry in Africa Growth

Key growth factors include increased investment in manufacturing capacity, government initiatives promoting local production, and the growing adoption of sustainable packaging solutions. Technological advancements, particularly in automation and digital printing, are further boosting efficiency and innovation. Also significant is growing consumer preference for convenience, safety and freshness.

Long-Term Growth Catalysts in the Packaging Industry in Africa

Long-term growth will be fueled by continued economic development, infrastructure improvements, and the rising adoption of sustainable packaging practices. Strategic partnerships between local and international players will play a crucial role in technology transfer and capacity building. The increasing focus on food safety and hygiene will further drive the demand for high-quality packaging solutions.

Emerging Opportunities in Packaging Industry in Africa

Opportunities exist in specialized packaging solutions for the healthcare and agricultural sectors, as well as in the development of innovative eco-friendly materials. The expansion of e-commerce continues to create demand for innovative packaging solutions that protect products during transit. Furthermore, there is an opportunity for companies to focus on packaging solutions for specific regional consumer needs.

Leading Players in the Packaging Industry in Africa Sector

- Frigoglass South Africa (Pty) Ltd

- Foster Packaging

- Nampak Limited

- Constantia Afripack (Pty) Ltd

- Consol Glass (Pty) Ltd

- Mondi Group

- Tetra Pak SA

- Astrapak Ltd (RPC Group)

- East African Packaging Industries Ltd (EAPI)

- Mpact Pty Ltd

- Bonpak (Pty) Ltd

Key Milestones in Packaging Industry in Africa Industry

- April 2022: Ardagh Group acquires Consol Holdings Proprietary Limited for USD 1 billion, signaling significant investment in the African glass packaging market. A further USD 200 million investment is planned for new furnaces.

- June 2022: Dow expands its Project REFLEX flexible packaging recycling initiative to Egypt and Guinea, promoting sustainable practices in waste management.

Strategic Outlook for Packaging Industry in Africa Market

The African packaging industry offers substantial growth potential driven by increasing consumer demand, favorable demographics, and ongoing investments in infrastructure. Companies that embrace sustainable practices, leverage technological advancements, and adapt to local market needs will be best positioned to capitalize on this opportunity. Strategic partnerships and collaborations will be critical for navigating regulatory landscapes and fostering innovation.

Packaging Industry in Africa Segmentation

-

1. Material

- 1.1. Paper and Paperboard

- 1.2. Plastic

- 1.3. Metal

- 1.4. Glass

-

2. Product Type

- 2.1. Plastic Bottles

- 2.2. Glass Bottles

- 2.3. Corrugated Boxes

- 2.4. Metal Cans

- 2.5. Other Applications

-

3. End-user Industry

- 3.1. Beverage

- 3.2. Food

- 3.3. Pharmaceuticals

- 3.4. Household and Personal Care

- 3.5. Other

Packaging Industry in Africa Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Packaging Industry in Africa Regional Market Share

Geographic Coverage of Packaging Industry in Africa

Packaging Industry in Africa REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Paper and Paperboard

- 5.1.2. Plastic

- 5.1.3. Metal

- 5.1.4. Glass

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Plastic Bottles

- 5.2.2. Glass Bottles

- 5.2.3. Corrugated Boxes

- 5.2.4. Metal Cans

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Beverage

- 5.3.2. Food

- 5.3.3. Pharmaceuticals

- 5.3.4. Household and Personal Care

- 5.3.5. Other

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Packaging Industry in Africa Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Paper and Paperboard

- 6.1.2. Plastic

- 6.1.3. Metal

- 6.1.4. Glass

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Plastic Bottles

- 6.2.2. Glass Bottles

- 6.2.3. Corrugated Boxes

- 6.2.4. Metal Cans

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Beverage

- 6.3.2. Food

- 6.3.3. Pharmaceuticals

- 6.3.4. Household and Personal Care

- 6.3.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. North America Packaging Industry in Africa Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Paper and Paperboard

- 7.1.2. Plastic

- 7.1.3. Metal

- 7.1.4. Glass

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Plastic Bottles

- 7.2.2. Glass Bottles

- 7.2.3. Corrugated Boxes

- 7.2.4. Metal Cans

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Beverage

- 7.3.2. Food

- 7.3.3. Pharmaceuticals

- 7.3.4. Household and Personal Care

- 7.3.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. South America Packaging Industry in Africa Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Paper and Paperboard

- 8.1.2. Plastic

- 8.1.3. Metal

- 8.1.4. Glass

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Plastic Bottles

- 8.2.2. Glass Bottles

- 8.2.3. Corrugated Boxes

- 8.2.4. Metal Cans

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Beverage

- 8.3.2. Food

- 8.3.3. Pharmaceuticals

- 8.3.4. Household and Personal Care

- 8.3.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Europe Packaging Industry in Africa Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Paper and Paperboard

- 9.1.2. Plastic

- 9.1.3. Metal

- 9.1.4. Glass

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Plastic Bottles

- 9.2.2. Glass Bottles

- 9.2.3. Corrugated Boxes

- 9.2.4. Metal Cans

- 9.2.5. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Beverage

- 9.3.2. Food

- 9.3.3. Pharmaceuticals

- 9.3.4. Household and Personal Care

- 9.3.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Middle East & Africa Packaging Industry in Africa Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Paper and Paperboard

- 10.1.2. Plastic

- 10.1.3. Metal

- 10.1.4. Glass

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Plastic Bottles

- 10.2.2. Glass Bottles

- 10.2.3. Corrugated Boxes

- 10.2.4. Metal Cans

- 10.2.5. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Beverage

- 10.3.2. Food

- 10.3.3. Pharmaceuticals

- 10.3.4. Household and Personal Care

- 10.3.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Asia Pacific Packaging Industry in Africa Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material

- 11.1.1. Paper and Paperboard

- 11.1.2. Plastic

- 11.1.3. Metal

- 11.1.4. Glass

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Plastic Bottles

- 11.2.2. Glass Bottles

- 11.2.3. Corrugated Boxes

- 11.2.4. Metal Cans

- 11.2.5. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Beverage

- 11.3.2. Food

- 11.3.3. Pharmaceuticals

- 11.3.4. Household and Personal Care

- 11.3.5. Other

- 11.1. Market Analysis, Insights and Forecast - by Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Frigoglass South Africa (Pty) Ltd *List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Foster Packaging

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Nampak Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Constantia Afripack (Pty) Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Consol Glass (Pty) Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Mondi Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Tetra Pak SA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Astrapak Ltd (RPC Group)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 East African Packaging Industries Ltd (EAPI)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mpact Pty Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Bonpak (Pty) Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Frigoglass South Africa (Pty) Ltd *List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Packaging Industry in Africa Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Packaging Industry in Africa Revenue (Million), by Material 2025 & 2033

- Figure 3: North America Packaging Industry in Africa Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Packaging Industry in Africa Revenue (Million), by Product Type 2025 & 2033

- Figure 5: North America Packaging Industry in Africa Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Packaging Industry in Africa Revenue (Million), by End-user Industry 2025 & 2033

- Figure 7: North America Packaging Industry in Africa Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Packaging Industry in Africa Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Packaging Industry in Africa Revenue Share (%), by Country 2025 & 2033

- Figure 10: South America Packaging Industry in Africa Revenue (Million), by Material 2025 & 2033

- Figure 11: South America Packaging Industry in Africa Revenue Share (%), by Material 2025 & 2033

- Figure 12: South America Packaging Industry in Africa Revenue (Million), by Product Type 2025 & 2033

- Figure 13: South America Packaging Industry in Africa Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: South America Packaging Industry in Africa Revenue (Million), by End-user Industry 2025 & 2033

- Figure 15: South America Packaging Industry in Africa Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: South America Packaging Industry in Africa Revenue (Million), by Country 2025 & 2033

- Figure 17: South America Packaging Industry in Africa Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Packaging Industry in Africa Revenue (Million), by Material 2025 & 2033

- Figure 19: Europe Packaging Industry in Africa Revenue Share (%), by Material 2025 & 2033

- Figure 20: Europe Packaging Industry in Africa Revenue (Million), by Product Type 2025 & 2033

- Figure 21: Europe Packaging Industry in Africa Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe Packaging Industry in Africa Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Europe Packaging Industry in Africa Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Europe Packaging Industry in Africa Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Packaging Industry in Africa Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East & Africa Packaging Industry in Africa Revenue (Million), by Material 2025 & 2033

- Figure 27: Middle East & Africa Packaging Industry in Africa Revenue Share (%), by Material 2025 & 2033

- Figure 28: Middle East & Africa Packaging Industry in Africa Revenue (Million), by Product Type 2025 & 2033

- Figure 29: Middle East & Africa Packaging Industry in Africa Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Middle East & Africa Packaging Industry in Africa Revenue (Million), by End-user Industry 2025 & 2033

- Figure 31: Middle East & Africa Packaging Industry in Africa Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Middle East & Africa Packaging Industry in Africa Revenue (Million), by Country 2025 & 2033

- Figure 33: Middle East & Africa Packaging Industry in Africa Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific Packaging Industry in Africa Revenue (Million), by Material 2025 & 2033

- Figure 35: Asia Pacific Packaging Industry in Africa Revenue Share (%), by Material 2025 & 2033

- Figure 36: Asia Pacific Packaging Industry in Africa Revenue (Million), by Product Type 2025 & 2033

- Figure 37: Asia Pacific Packaging Industry in Africa Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Asia Pacific Packaging Industry in Africa Revenue (Million), by End-user Industry 2025 & 2033

- Figure 39: Asia Pacific Packaging Industry in Africa Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Asia Pacific Packaging Industry in Africa Revenue (Million), by Country 2025 & 2033

- Figure 41: Asia Pacific Packaging Industry in Africa Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Packaging Industry in Africa Revenue Million Forecast, by Material 2020 & 2033

- Table 2: Global Packaging Industry in Africa Revenue Million Forecast, by Product Type 2020 & 2033

- Table 3: Global Packaging Industry in Africa Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Packaging Industry in Africa Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Packaging Industry in Africa Revenue Million Forecast, by Material 2020 & 2033

- Table 6: Global Packaging Industry in Africa Revenue Million Forecast, by Product Type 2020 & 2033

- Table 7: Global Packaging Industry in Africa Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Packaging Industry in Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Packaging Industry in Africa Revenue Million Forecast, by Material 2020 & 2033

- Table 13: Global Packaging Industry in Africa Revenue Million Forecast, by Product Type 2020 & 2033

- Table 14: Global Packaging Industry in Africa Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Packaging Industry in Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Brazil Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Argentina Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of South America Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Packaging Industry in Africa Revenue Million Forecast, by Material 2020 & 2033

- Table 20: Global Packaging Industry in Africa Revenue Million Forecast, by Product Type 2020 & 2033

- Table 21: Global Packaging Industry in Africa Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 22: Global Packaging Industry in Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 23: United Kingdom Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Germany Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: France Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Italy Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Spain Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Russia Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Benelux Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Nordics Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Europe Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Packaging Industry in Africa Revenue Million Forecast, by Material 2020 & 2033

- Table 33: Global Packaging Industry in Africa Revenue Million Forecast, by Product Type 2020 & 2033

- Table 34: Global Packaging Industry in Africa Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 35: Global Packaging Industry in Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Turkey Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Israel Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: GCC Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: North Africa Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: South Africa Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East & Africa Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Global Packaging Industry in Africa Revenue Million Forecast, by Material 2020 & 2033

- Table 43: Global Packaging Industry in Africa Revenue Million Forecast, by Product Type 2020 & 2033

- Table 44: Global Packaging Industry in Africa Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 45: Global Packaging Industry in Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 46: China Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 47: India Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Japan Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 49: South Korea Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: ASEAN Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 51: Oceania Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Rest of Asia Pacific Packaging Industry in Africa Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Packaging Industry in Africa?

The projected CAGR is approximately 3.85%.

2. Which companies are prominent players in the Packaging Industry in Africa?

Key companies in the market include Frigoglass South Africa (Pty) Ltd *List Not Exhaustive, Foster Packaging, Nampak Limited, Constantia Afripack (Pty) Ltd, Consol Glass (Pty) Ltd, Mondi Group, Tetra Pak SA, Astrapak Ltd (RPC Group), East African Packaging Industries Ltd (EAPI), Mpact Pty Ltd, Bonpak (Pty) Ltd.

3. What are the main segments of the Packaging Industry in Africa?

The market segments include Material, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 43.48 Million as of 2022.

5. What are some drivers contributing to market growth?

Glass Bottles to Drive the Market Growth; Beverage Industry to Lead the Market Growth.

6. What are the notable trends driving market growth?

Glass Bottles to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Fluctuation in Raw Material Price can Hinder the Growth of the Market..

8. Can you provide examples of recent developments in the market?

June 2022: Dow expanded the flexible packaging recycling initiative to new African markets. Dow announced that its flexible packaging recycling initiative, project REFLEX, will be expanded to Egypt and Guinea. The expansion of Project REFLEX into Egypt began in December 2021, with Dow entering an 18-month partnership with the international non-government organization, WasteAid, which shares waste management and recycling skills with lower- and middle-income countries. WasteAid will work with Dow to advance waste recovery and recycling in Aswan, a city located in southern Egypt.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Packaging Industry in Africa," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Packaging Industry in Africa report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Packaging Industry in Africa?

To stay informed about further developments, trends, and reports in the Packaging Industry in Africa, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence