Key Insights

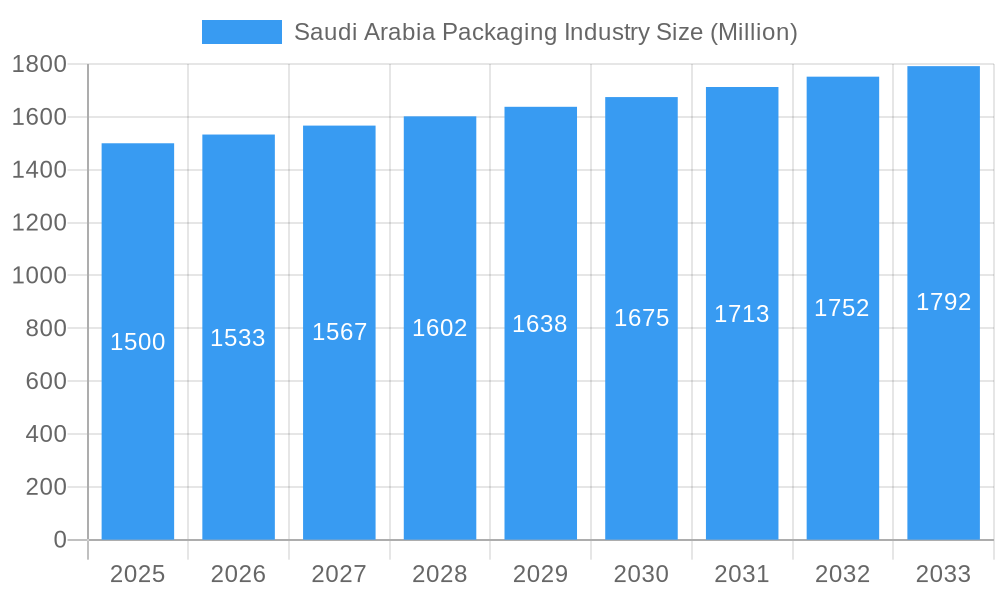

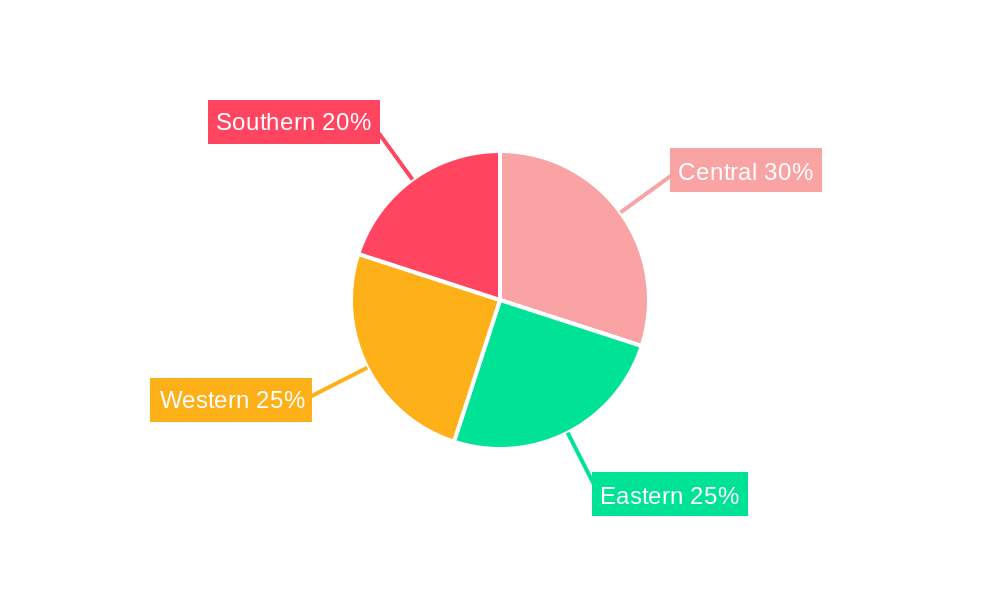

The Saudi Arabian packaging market is poised for significant expansion, projected to reach $14.81 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.62% from 2025 to 2033. This growth trajectory is propelled by several dynamic factors. The rapidly expanding food and beverage sector, driven by demographic shifts and rising consumer spending power, is a primary catalyst for diverse packaging demands. Concurrently, the healthcare and pharmaceutical industries are witnessing substantial growth, requiring advanced and secure packaging solutions. The burgeoning e-commerce landscape further fuels market expansion, necessitating durable and efficient packaging for online retail logistics. A prominent emerging trend is the increasing adoption of sustainable packaging, spurred by environmental consciousness and regulatory mandates, leading to greater investment in eco-friendly materials such as biodegradable plastics and recycled paper. Potential market restraints include raw material price volatility and economic uncertainties. The market's segmentation across flexible and rigid packaging, diverse materials including plastic, glass, and metal, and a wide array of end-user industries highlights multifaceted opportunities for specialized packaging providers. The competitive environment is characterized by a strong presence of both domestic and international players, including Almoayyed International Group, Sapin, and Amcor PLC, who are actively pursuing distinct strategies to capture market share. Regional demand variations are evident across Saudi Arabia's central, eastern, western, and southern regions, reflecting differences in population density and economic activity.

Saudi Arabia Packaging Industry Market Size (In Billion)

The future outlook for the Saudi Arabian packaging market is highly promising. Continued investment in infrastructure, encompassing logistics and distribution networks, will amplify demand for advanced packaging solutions. Government initiatives aimed at economic diversification and supporting local enterprises will further bolster the industry's growth. Sustained expansion will be contingent on adapting to evolving consumer preferences, adhering to stringent environmental regulations, and effectively navigating global economic complexities. Strategic imperatives will focus on material and design innovation, ensuring strict adherence to safety and environmental standards, and fortifying supply chains to meet the escalating demands of a diverse industrial base. These factors present significant opportunities for both established industry leaders and emerging businesses within the Saudi Arabian packaging sector.

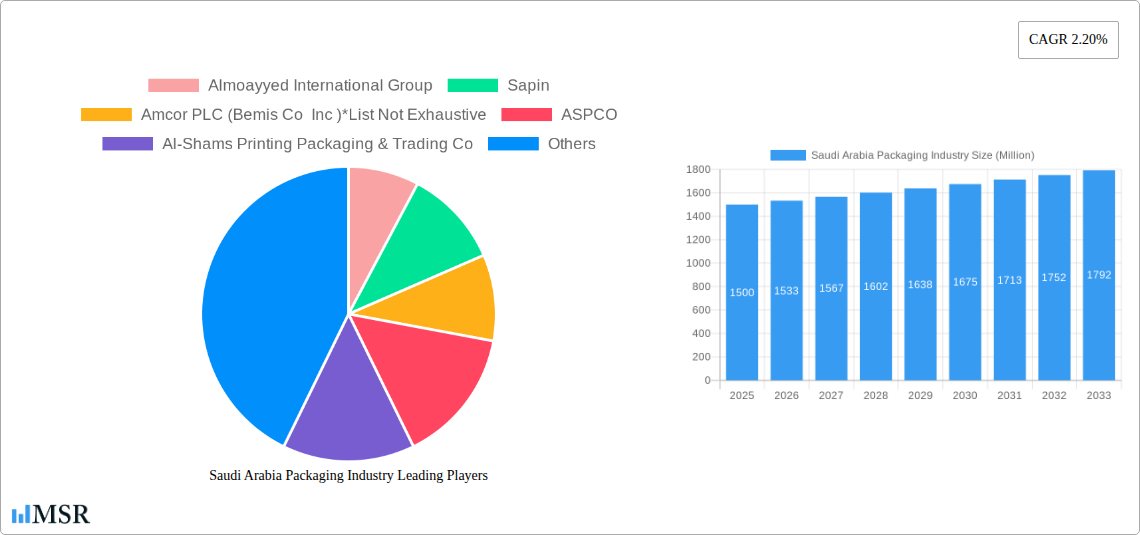

Saudi Arabia Packaging Industry Company Market Share

Saudi Arabia Packaging Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Saudi Arabia packaging industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report meticulously examines market size, growth drivers, key segments, competitive landscape, and future opportunities. The report is essential reading for investors, manufacturers, suppliers, and anyone involved in the Kingdom's thriving packaging sector. The market value is projected to reach xx Million by 2033, exhibiting a robust CAGR.

Saudi Arabia Packaging Industry Market Concentration & Dynamics

The Saudi Arabian packaging market exhibits a moderately concentrated landscape, with a handful of major players holding significant market share. Almoayyed International Group, Sapin, Amcor PLC (Bemis Co Inc), ASPCO, Al-Shams Printing Packaging & Trading Co, Napco National, PRINTOPACK, and PACFORT represent some of the key players. However, a considerable number of smaller, specialized companies also contribute to the overall market.

- Market Share: The top 5 players collectively hold an estimated 45% market share, indicating the presence of both large multinational corporations and strong domestic companies.

- Innovation Ecosystem: The industry shows a growing focus on sustainable packaging solutions, driven by government initiatives and consumer demand. However, investment in R&D remains an area for potential improvement.

- Regulatory Framework: Regulations concerning food safety and environmental compliance are becoming increasingly stringent, impacting packaging material choices and manufacturing processes.

- Substitute Products: The market faces competition from alternative packaging materials and evolving consumer preferences for sustainable options.

- End-User Trends: The growth of e-commerce and changing consumer lifestyles are impacting packaging demands, driving a need for innovative and convenient solutions.

- M&A Activities: The number of M&A deals in the Saudi Arabian packaging industry averaged 5 per year during the historical period (2019-2024), indicating strategic consolidation within the sector.

Saudi Arabia Packaging Industry Industry Insights & Trends

The Saudi Arabian packaging market is experiencing robust growth, fueled by several key factors. The expanding food and beverage sector, coupled with rising disposable incomes and a growing population, creates substantial demand for various packaging types. Furthermore, the burgeoning healthcare and pharmaceutical industries, along with the growth of the e-commerce sector, contribute to market expansion. The market size reached xx Million in 2024 and is projected to reach xx Million by 2025, growing at a xx% CAGR during the forecast period. Technological advancements, like the adoption of automation and smart packaging, are transforming the industry, while evolving consumer preferences towards convenience and sustainability are driving innovation. Key challenges include fluctuating raw material prices and the need for enhanced supply chain efficiency.

Key Markets & Segments Leading Saudi Arabia Packaging Industry

The Saudi Arabian packaging market is segmented by packaging type (flexible and rigid), packaging material (plastic, glass, metal, and others), and end-user industry (food, beverage, healthcare, retail, beauty, and others).

- By Packaging Type: Flexible packaging currently holds the largest market share, driven by its cost-effectiveness and versatility. Rigid packaging is also experiencing significant growth due to increased demand from the food and beverage sectors.

- By Packaging Material: Plastic dominates the market due to its affordability and versatility. However, the increasing focus on sustainability is driving growth in alternative materials like paperboard and biodegradable plastics.

- By End-user Industry: The food and beverage sector is the largest consumer of packaging, followed by the healthcare and retail sectors. The growth of these industries is directly driving packaging demand.

Drivers for Dominant Segments:

- Economic Growth: Sustained economic growth in Saudi Arabia is directly fueling demand for various packaging solutions.

- Infrastructure Development: Improved infrastructure facilitates efficient supply chain operations, supporting the growth of the industry.

- Population Growth: The increasing population fuels higher demand for packaged goods in various sectors.

Saudi Arabia Packaging Industry Product Developments

Recent years have witnessed significant product innovations in the Saudi Arabian packaging industry. Advancements in flexible packaging materials, including the use of barrier films and modified atmosphere packaging (MAP), are enhancing product shelf life and preserving quality. The adoption of sustainable packaging materials, like recycled plastics and biodegradable alternatives, is gaining momentum, reflecting a growing commitment to environmental responsibility. Furthermore, smart packaging technologies, incorporating features such as sensors and RFID tags, are emerging as promising developments, providing traceability and enhancing consumer experience.

Challenges in the Saudi Arabia Packaging Industry Market

Several challenges hinder the growth of the Saudi Arabian packaging market. Fluctuating raw material prices, particularly for plastics and polymers, significantly impact profitability. Supply chain disruptions and logistical complexities add to the challenges. The increasing competition from both domestic and international players intensifies the pressure on pricing and margins. Furthermore, complying with stringent environmental regulations related to waste management and recycling poses a challenge for many companies. The combined effect of these factors contributes to a need for innovation in sourcing, manufacturing, and waste management.

Forces Driving Saudi Arabia Packaging Industry Growth

Several factors drive the long-term growth of the Saudi Arabian packaging industry. Government initiatives promoting the growth of key sectors like food processing and healthcare create significant demand. The increasing adoption of e-commerce and online retail necessitates efficient and secure packaging solutions. Furthermore, continuous technological advancements in packaging materials and automation contribute to overall efficiency and innovation. These factors provide a strong foundation for the industry's continued expansion.

Long-Term Growth Catalysts in the Saudi Arabia Packaging Industry

The Saudi Vision 2030 initiatives focused on economic diversification and sustainable development create a favorable climate for the packaging sector. Strategic partnerships between local and international players will boost innovation and technology transfer. Market expansion into new segments, such as personalized packaging and customized solutions, presents further growth potential. The focus on sustainability and the increasing adoption of eco-friendly packaging solutions will shape future market dynamics.

Emerging Opportunities in Saudi Arabia Packaging Industry

The adoption of sustainable and eco-friendly packaging materials presents significant opportunities. The growth of e-commerce continues to drive demand for protective and convenient packaging solutions. The increasing demand for specialized packaging in sectors like pharmaceuticals and cosmetics creates niche market possibilities. Innovations in smart packaging, integrating technology for traceability and consumer engagement, offer significant potential for growth.

Leading Players in the Saudi Arabia Packaging Industry Sector

- Almoayyed International Group

- Sapin

- Amcor PLC (Bemis Co Inc)

- ASPCO

- Al-Shams Printing Packaging & Trading Co

- Napco National

- PRINTOPACK

- PACFORT

Key Milestones in Saudi Arabia Packaging Industry Industry

- 2020: Introduction of stricter environmental regulations concerning plastic waste management.

- 2021: Several major players invested in advanced automation technologies for improved efficiency.

- 2022: Launch of a significant number of new sustainable packaging solutions by leading companies.

- 2023: Several M&A activities consolidated the market share of key players.

- 2024: Government incentives for the adoption of smart packaging technologies were announced.

Strategic Outlook for Saudi Arabia Packaging Industry Market

The Saudi Arabian packaging industry is poised for continued growth, driven by sustained economic expansion, demographic changes, and technological advancements. Strategic investments in sustainable packaging solutions, automation, and e-commerce-focused packaging will be crucial for success. The focus on building strong supply chain partnerships and adapting to evolving consumer preferences will be key to unlocking future market potential. The industry's long-term prospects appear robust, given the Kingdom's ongoing economic development and commitment to sustainable growth.

Saudi Arabia Packaging Industry Segmentation

-

1. Packaging Type

- 1.1. Flexible Packaging

- 1.2. Rigid Packaging

-

2. Packaging Material

- 2.1. Plastic

- 2.2. Glass

- 2.3. Metal

- 2.4. Other Packaging Materials

-

3. End-user Industry

- 3.1. Food

- 3.2. Beverage

- 3.3. Healthcare and Pharmaceutical

- 3.4. Retail

- 3.5. Beauty and Personal Care

- 3.6. Other End-user Industries

Saudi Arabia Packaging Industry Segmentation By Geography

- 1. Saudi Arabia

Saudi Arabia Packaging Industry Regional Market Share

Geographic Coverage of Saudi Arabia Packaging Industry

Saudi Arabia Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 5.1.1. Flexible Packaging

- 5.1.2. Rigid Packaging

- 5.2. Market Analysis, Insights and Forecast - by Packaging Material

- 5.2.1. Plastic

- 5.2.2. Glass

- 5.2.3. Metal

- 5.2.4. Other Packaging Materials

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Beverage

- 5.3.3. Healthcare and Pharmaceutical

- 5.3.4. Retail

- 5.3.5. Beauty and Personal Care

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6. Saudi Arabia Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6.1.1. Flexible Packaging

- 6.1.2. Rigid Packaging

- 6.2. Market Analysis, Insights and Forecast - by Packaging Material

- 6.2.1. Plastic

- 6.2.2. Glass

- 6.2.3. Metal

- 6.2.4. Other Packaging Materials

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Beverage

- 6.3.3. Healthcare and Pharmaceutical

- 6.3.4. Retail

- 6.3.5. Beauty and Personal Care

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Almoayyed International Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sapin

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Amcor PLC (Bemis Co Inc )*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ASPCO

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Al-Shams Printing Packaging & Trading Co

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Napco National

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 PRINTOPACK

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PACFORT

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Almoayyed International Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Saudi Arabia Packaging Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Saudi Arabia Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Saudi Arabia Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 2: Saudi Arabia Packaging Industry Revenue billion Forecast, by Packaging Material 2020 & 2033

- Table 3: Saudi Arabia Packaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Saudi Arabia Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Saudi Arabia Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 6: Saudi Arabia Packaging Industry Revenue billion Forecast, by Packaging Material 2020 & 2033

- Table 7: Saudi Arabia Packaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Saudi Arabia Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Saudi Arabia Packaging Industry?

The projected CAGR is approximately 5.62%.

2. Which companies are prominent players in the Saudi Arabia Packaging Industry?

Key companies in the market include Almoayyed International Group, Sapin, Amcor PLC (Bemis Co Inc )*List Not Exhaustive, ASPCO, Al-Shams Printing Packaging & Trading Co, Napco National, PRINTOPACK, PACFORT.

3. What are the main segments of the Saudi Arabia Packaging Industry?

The market segments include Packaging Type, Packaging Material, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.81 billion as of 2022.

5. What are some drivers contributing to market growth?

; Urbanization in the Country; Increased Foreign Direct Investments.

6. What are the notable trends driving market growth?

Rigid Packaging Materials. like Paper and Paperboard. are Expected to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

; Reforms to Control the Use of Plastic Packaging.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Saudi Arabia Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Saudi Arabia Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Saudi Arabia Packaging Industry?

To stay informed about further developments, trends, and reports in the Saudi Arabia Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence