Key Insights

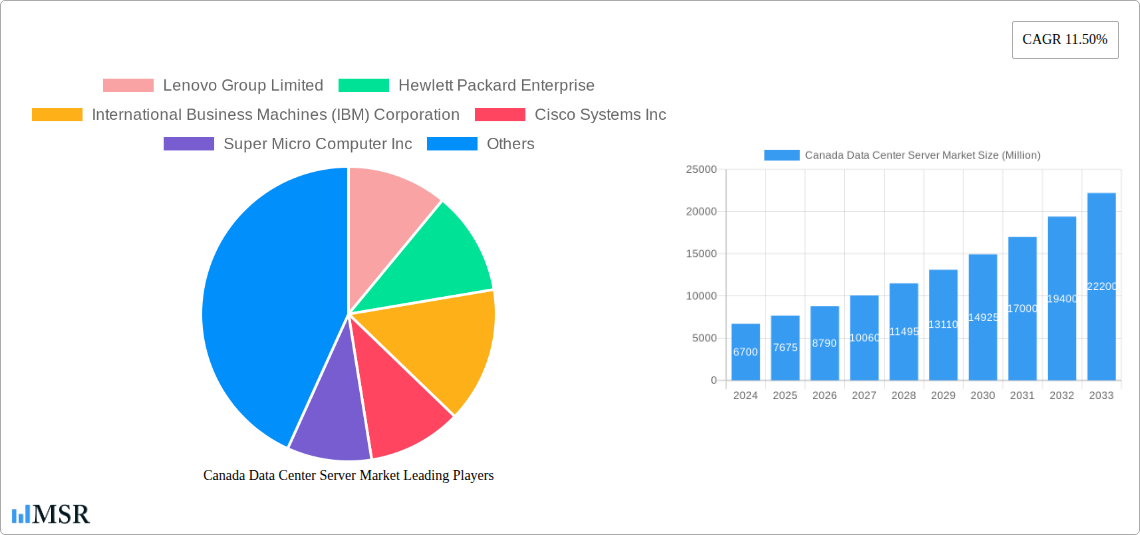

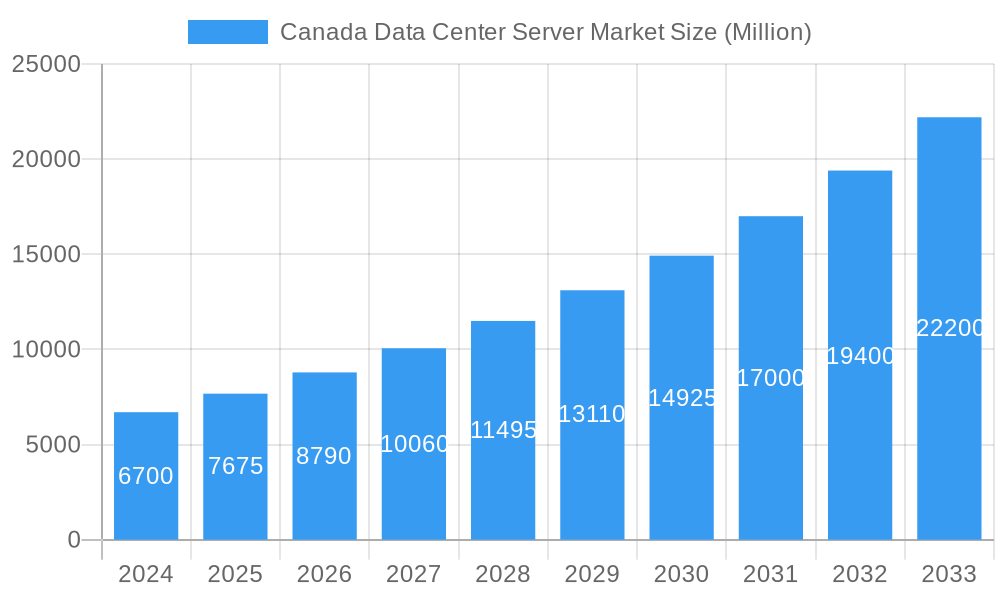

The Canadian data center server market is poised for significant expansion, driven by escalating digital transformation initiatives and the burgeoning demand for robust IT infrastructure. With a projected market size of $6.70 billion in 2024, the sector is on track to experience a remarkable 14.54% CAGR through 2033. This robust growth is primarily fueled by the increasing adoption of cloud computing, the proliferation of big data analytics, and the continuous need for enhanced processing power to support emerging technologies like AI and IoT. Key end-user segments, including the IT & Telecommunication sector, BFSI (Banking, Financial Services, and Insurance), and Government, are leading this charge, investing heavily in advanced server solutions to manage their growing data volumes and ensure operational efficiency. The continuous evolution of technologies such as AI, machine learning, and edge computing is creating a sustained demand for high-performance, scalable, and energy-efficient server hardware.

Canada Data Center Server Market Market Size (In Billion)

The competitive landscape in the Canadian data center server market is characterized by the presence of global technology giants and specialized players. Companies like Lenovo, Hewlett Packard Enterprise, and IBM are actively competing, offering a diverse range of server form factors, from blade and rack servers to tower servers, to cater to varied enterprise needs. Emerging trends such as the increasing focus on sustainability and energy efficiency in data center operations, coupled with the growing adoption of specialized servers for AI and high-performance computing (HPC), are shaping market dynamics. While growth is robust, potential restraints include the high initial investment costs for advanced server infrastructure and concerns around cybersecurity and data privacy, which may necessitate careful planning and investment in robust security measures. Nevertheless, the overall outlook remains exceptionally positive, with substantial opportunities for innovation and market penetration.

Canada Data Center Server Market Company Market Share

Canada Data Center Server Market Report: Unlocking the Future of Cloud Infrastructure & AI Compute

This comprehensive report dives deep into the Canada data center server market, forecasting significant growth driven by the surging demand for Artificial Intelligence (AI), robust cloud adoption, and the digital transformation across critical industries. The Canadian server market is poised for expansion, with the Canada data center server market size projected to reach $XX billion by 2033, exhibiting a compound annual growth rate (CAGR) of XX% during the forecast period of 2025–2033. This in-depth analysis provides actionable insights for stakeholders looking to capitalize on the evolving data center infrastructure Canada landscape, focusing on server solutions Canada, enterprise servers Canada, and AI server market Canada.

Canada Data Center Server Market Market Concentration & Dynamics

The Canada data center server market is characterized by a moderate level of concentration, with a mix of global giants and emerging players vying for market share. Key companies such as Lenovo Group Limited, Hewlett Packard Enterprise, International Business Machines (IBM) Corporation, Cisco Systems Inc, Super Micro Computer Inc, Dell Inc, Quanta Computer Inc, Kingston Technology Company Inc, Inspur Group, and Huawei Technologies Co Ltd are actively shaping the competitive landscape through innovation and strategic partnerships. The market's innovation ecosystem is vibrant, fueled by ongoing advancements in AI, high-performance computing (HPC), and edge computing, which necessitate more powerful and specialized server architectures. Regulatory frameworks, while generally supportive of technological advancement, are increasingly focusing on data privacy and security, influencing server design and deployment strategies. Substitute products, such as cloud-based services, continue to present a competitive dynamic, yet the dedicated hardware requirements for specific AI workloads and on-premises data sovereignty needs ensure continued demand for physical servers. End-user trends, particularly the rapid adoption of Generative AI (GenAI) and the expanding digital footprint of businesses, are creating significant new opportunities. Mergers and acquisitions (M&A) activities, while not as frequent as in some other tech sectors, are strategic moves to consolidate market presence and acquire specialized technological capabilities, with an estimated XX M&A deals recorded in the historical period.

Canada Data Center Server Market Industry Insights & Trends

The Canada data center server market is experiencing a transformative period, with numerous factors propelling its growth. The escalating demand for computing power to support Generative AI (GenAI) applications is a primary driver. The paradigm shift in IT planning, as evidenced by Dell's launch of modular, full-stack AI solutions in July 2023, highlights the enterprise need for secure, high-performance architectures for deploying large language models (LLMs). This has consequently spurred a strong demand for GPU accelerator servers, essential for the computationally intensive training and inferencing of GenAI workflows. Furthermore, the continuous push for digital transformation across all sectors, including IT & Telecommunication, BFSI (Banking, Financial Services, and Insurance), Government, and Media & Entertainment, necessitates upgrades and expansions of existing data center infrastructure. Cloud computing, while a substitute in some contexts, also acts as a significant growth driver for server hardware as cloud providers scale their offerings. Cisco's demonstration of reducing data center energy consumption by up to 52 percent with its UCS X-Series servers and Intersight platform in May 2023 showcases the industry's focus on efficiency and sustainability, which are becoming increasingly important considerations for server procurement. The increasing prevalence of IoT devices and the growing volume of data generated by these devices are also contributing to the demand for robust server solutions capable of handling large-scale data processing and analytics. The market size is estimated to be around $XX billion in 2025, with robust growth projected over the forecast period.

Key Markets & Segments Leading Canada Data Center Server Market

The Canada data center server market is experiencing dominant growth across several key segments and end-users.

Form Factor Dominance:

- Rack Servers: Currently holding the largest market share, rack servers remain the backbone of most data centers due to their versatility, scalability, and cost-effectiveness. Their modular design allows for easy integration and expansion, making them ideal for a wide range of applications from general computing to specialized AI workloads. The economic growth in Canada and the widespread adoption of cloud services continue to drive demand for rack servers.

- Blade Servers: Gaining significant traction, blade servers are increasingly favored for their high-density computing capabilities, power efficiency, and simplified management. They are particularly crucial for organizations with space and power constraints, and for high-performance computing (HPC) environments. The ongoing development of advanced cooling technologies and power management solutions further enhances their appeal.

- Tower Servers: While typically serving smaller businesses or specific departmental needs, tower servers continue to play a role in the Canadian market, especially for organizations that do not require the centralized infrastructure of a traditional data center.

End-User Dominance:

- IT & Telecommunication: This sector is the leading consumer of data center servers in Canada. The relentless demand for bandwidth, cloud services, 5G deployment, and digital content delivery necessitates continuous investment in high-performance server infrastructure. The rapid pace of technological innovation within this industry fuels consistent demand for cutting-edge server solutions.

- BFSI (Banking, Financial Services, and Insurance): The BFSI sector is a major driver of the Canada enterprise server market. With increasing digitization of financial services, the need for secure, reliable, and high-performance servers for transaction processing, data analytics, risk management, and fraud detection is paramount. The stringent regulatory requirements for data security and compliance further bolster the demand for robust server solutions.

- Government: Government agencies are significantly investing in modernizing their IT infrastructure to improve service delivery, enhance national security, and manage vast amounts of data. This includes the adoption of cloud technologies and the deployment of specialized servers for various public sector applications, driving demand for government servers Canada.

- Media & Entertainment: The exponential growth in streaming services, digital content creation, and immersive technologies (like VR/AR) requires substantial processing power and storage. This segment's increasing reliance on data-intensive applications is a key growth catalyst for the Canada data center server market.

Canada Data Center Server Market Product Developments

The Canada data center server market is witnessing a rapid evolution in product development, with a strong emphasis on AI and energy efficiency. Dell's July 2023 launch of Generative Artificial Intelligence Solutions, featuring a modular, full-stack architecture, directly addresses the growing need for secure and high-performance AI server solutions Canada for deploying LLMs. This signifies a broader industry trend towards specialized hardware designed for computational-intensive AI workloads, including a surge in demand for GPU accelerator servers. Simultaneously, innovations like Cisco's May 2023 announcement showcasing up to 52% reduction in data center energy consumption by combining their Intersight platform with UCS X-Series servers underscore the market's commitment to sustainable and efficient data center infrastructure Canada. These advancements are not only enhancing processing capabilities but also addressing critical environmental concerns, giving companies a competitive edge.

Challenges in the Canada Data Center Server Market Market

The Canada data center server market faces several challenges that impact its growth trajectory. Regulatory hurdles, particularly concerning data sovereignty and privacy, can impose complex compliance requirements and influence purchasing decisions. Supply chain disruptions, as experienced globally, can lead to increased lead times and costs for essential server components, affecting project timelines and budget predictability. Furthermore, intense competitive pressures from both established global vendors and emerging players can lead to price erosion and necessitate continuous innovation to maintain market share. The cost of high-performance components, especially GPUs for AI workloads, also presents a significant barrier for some organizations.

Forces Driving Canada Data Center Server Market Growth

Several powerful forces are driving the growth of the Canada data center server market. The relentless surge in demand for Artificial Intelligence (AI) and Machine Learning (ML) applications, particularly Generative AI, is a primary catalyst, requiring substantial computational power. The ongoing digital transformation across industries like BFSI, healthcare, and government necessitates robust and scalable server infrastructure. Furthermore, the expansion of cloud computing services, both public and private, fuels the demand for advanced enterprise servers Canada to power these platforms. Government initiatives aimed at fostering innovation and digital infrastructure also contribute significantly to market expansion.

Challenges in the Canada Data Center Server Market Market

The Canada data center server market is characterized by long-term growth catalysts including the accelerating adoption of edge computing, which requires localized processing power and thus specialized servers. The increasing focus on sustainable and energy-efficient server technologies is another significant catalyst, driving demand for innovative cooling solutions and power management systems. Furthermore, the continuous evolution of cybersecurity threats necessitates regular hardware upgrades and the deployment of servers with enhanced security features. Strategic partnerships and collaborations between hardware manufacturers, software providers, and cloud service providers are also fostering market growth by creating integrated and comprehensive solutions.

Emerging Opportunities in Canada Data Center Server Market

Emerging opportunities in the Canada data center server market are abundant and diverse. The burgeoning field of quantum computing, while nascent, presents a long-term potential for specialized high-performance computing servers. The increasing adoption of edge computing solutions for IoT devices and real-time data processing in sectors like manufacturing and logistics creates a demand for compact, powerful, and resilient servers. Furthermore, the growing emphasis on hybrid and multi-cloud strategies by enterprises opens up opportunities for vendors offering flexible and interoperable server solutions that can seamlessly integrate across different cloud environments. The development of specialized servers for edge AI applications is also a significant emerging trend.

Leading Players in the Canada Data Center Server Market Sector

- Lenovo Group Limited

- Hewlett Packard Enterprise

- International Business Machines (IBM) Corporation

- Cisco Systems Inc

- Super Micro Computer Inc

- Dell Inc

- Quanta Computer Inc

- Kingston Technology Company Inc

- Inspur Group

- Huawei Technologies Co Ltd

Key Milestones in Canada Data Center Server Market Industry

- July 2023: Dell launched Generative Artificial Intelligence Solutions, offering a modular, full-stack architecture for enterprises seeking a secure, high-performance, proven architecture for deploying large language models (LLM). This marked a significant advancement in addressing the burgeoning demand for AI infrastructure, particularly for GPU accelerator servers crucial for GenAI workflows.

- May 2023: Cisco announced that by combining its Intersight infrastructure management platform with Unified Computing System (UCS) X-Series servers, it can reduce data center energy consumption by up to 52 percent at a four-to-one (4:1) server consolidation ratio. This development highlights the increasing industry focus on energy efficiency and sustainable data center operations, influencing server design and deployment strategies.

Strategic Outlook for Canada Data Center Server Market Market

The strategic outlook for the Canada data center server market is exceptionally positive, driven by the indispensable role of servers in powering AI, cloud computing, and digital transformation initiatives. The market is poised for sustained growth, with companies focusing on enhancing performance, energy efficiency, and security in their server offerings. Strategic investments in research and development for AI-optimized hardware, alongside the expansion of cloud and edge computing infrastructure, will be critical. Partnerships that foster innovation and provide integrated solutions will also play a pivotal role. The increasing demand for specialized GPU servers Canada and robust enterprise servers Canada presents significant opportunities for market participants to capture substantial market share in the coming years.

Canada Data Center Server Market Segmentation

-

1. Form Factor

- 1.1. Blade Server

- 1.2. Rack Server

- 1.3. Tower Server

-

2. End-User

- 2.1. IT & Telecommunication

- 2.2. BFSI

- 2.3. Government

- 2.4. Media & Entertainment

- 2.5. Other End-User

Canada Data Center Server Market Segmentation By Geography

- 1. Canada

Canada Data Center Server Market Regional Market Share

Geographic Coverage of Canada Data Center Server Market

Canada Data Center Server Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Number of Smartpone Users; Fiber Connectivity Network Expansion

- 3.3. Market Restrains

- 3.3.1. Increasing number of Data Security Breaches

- 3.4. Market Trends

- 3.4.1. IT & Telecommunication Is The Largest Market In The Country

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Data Center Server Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Form Factor

- 5.1.1. Blade Server

- 5.1.2. Rack Server

- 5.1.3. Tower Server

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. IT & Telecommunication

- 5.2.2. BFSI

- 5.2.3. Government

- 5.2.4. Media & Entertainment

- 5.2.5. Other End-User

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Form Factor

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Lenovo Group Limited

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Hewlett Packard Enterprise

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 International Business Machines (IBM) Corporation

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Cisco Systems Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Super Micro Computer Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Dell Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Quanta Computer Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Kingston Technology Company Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Inspur Group

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Huawei Technologies Co Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Lenovo Group Limited

List of Figures

- Figure 1: Canada Data Center Server Market Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Canada Data Center Server Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Data Center Server Market Revenue undefined Forecast, by Form Factor 2020 & 2033

- Table 2: Canada Data Center Server Market Revenue undefined Forecast, by End-User 2020 & 2033

- Table 3: Canada Data Center Server Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Canada Data Center Server Market Revenue undefined Forecast, by Form Factor 2020 & 2033

- Table 5: Canada Data Center Server Market Revenue undefined Forecast, by End-User 2020 & 2033

- Table 6: Canada Data Center Server Market Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Data Center Server Market?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Canada Data Center Server Market?

Key companies in the market include Lenovo Group Limited, Hewlett Packard Enterprise, International Business Machines (IBM) Corporation, Cisco Systems Inc, Super Micro Computer Inc, Dell Inc, Quanta Computer Inc, Kingston Technology Company Inc, Inspur Group, Huawei Technologies Co Ltd.

3. What are the main segments of the Canada Data Center Server Market?

The market segments include Form Factor, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Number of Smartpone Users; Fiber Connectivity Network Expansion.

6. What are the notable trends driving market growth?

IT & Telecommunication Is The Largest Market In The Country.

7. Are there any restraints impacting market growth?

Increasing number of Data Security Breaches.

8. Can you provide examples of recent developments in the market?

July 2023: Dell launched Generative Artificial Intelligence Solutions that offers a modular, full-stack architecture for enterprises seeking a secure, high-performance, proven architecture for deploying large language models (LLM). A paradigm shift in IT planning has taken place due to the rapid demand for GenAI at work, which will continue to ripple through the industry. Thus, there has been a strong demand for graphics processing unit (GPU) accelerator servers that are driving the computational intensive training and inferencing of GenAI workflows.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Data Center Server Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Data Center Server Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Data Center Server Market?

To stay informed about further developments, trends, and reports in the Canada Data Center Server Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence