Key Insights

The biopolymer packaging market is experiencing robust growth, driven by increasing consumer demand for eco-friendly alternatives to traditional petroleum-based plastics. A compound annual growth rate (CAGR) of 12.60% from 2019 to 2024 suggests a significant market expansion, projected to continue into the forecast period (2025-2033). Key drivers include stringent government regulations aimed at reducing plastic waste, rising environmental awareness among consumers, and the growing adoption of sustainable packaging practices across various industries. The food and beverage sector, followed by retail and healthcare, are major end-user industries propelling market growth. Biodegradable materials are gaining significant traction, outpacing the growth of non-biodegradable options, reflecting a strong market shift towards environmentally responsible packaging solutions. While the market faces challenges such as higher production costs compared to conventional plastics and the need for improved biopolymer properties to match the performance of traditional materials, these hurdles are being actively addressed through technological advancements and innovative material formulations. Geographic analysis reveals strong market penetration in North America and Europe, with significant growth potential in the Asia-Pacific region driven by increasing industrialization and a rising middle class. Companies such as United Biopolymers SA, Taghleef Industries Inc., and Amcor PLC are key players shaping market dynamics through innovation and strategic partnerships. The market's future growth hinges on continued technological advancements in biopolymer production, expansion into new applications, and the ongoing development of robust recycling infrastructure to support a circular economy model for biopolymer packaging.

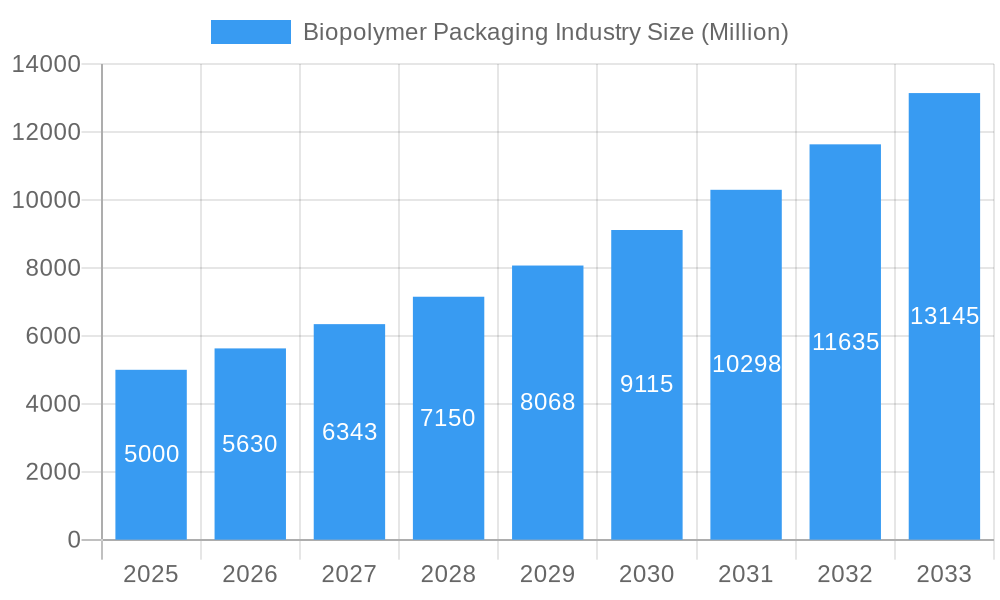

Biopolymer Packaging Industry Market Size (In Billion)

The projected market size for 2025, extrapolated from the provided data and industry trends, indicates a substantial valuation in the billions. The precise figure requires more detailed data, but the consistent high CAGR reflects significant potential. The continued growth throughout the forecast period (2025-2033) is expected to be influenced by ongoing legislative changes further incentivizing biopolymer adoption, particularly in regions with strong environmental protection policies. Furthermore, the increasing consumer preference for sustainable products will likely drive further market expansion. The competitive landscape remains dynamic, with continuous innovation and mergers & acquisitions shaping the industry. Market segmentation by material type and end-user industry will continue to evolve, with biodegradable materials and specific end-user sectors (like food and beverage) showing the strongest future growth.

Biopolymer Packaging Industry Company Market Share

Biopolymer Packaging Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Biopolymer Packaging Industry, offering invaluable insights for stakeholders, investors, and industry professionals. Covering the period from 2019 to 2033, with a focus on 2025, this report unveils market dynamics, growth drivers, key players, and future opportunities within this rapidly evolving sector. The global biopolymer packaging market size was valued at xx Million in 2024 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033).

Biopolymer Packaging Industry Market Concentration & Dynamics

The biopolymer packaging market presents a moderately concentrated landscape, dominated by several key players holding substantial market share. Prominent companies include United Biopolymers SA, Taghleef Industries Inc, Sonoco Products Company, Constantia Flexibles Group GmbH, Clondalkin Group Holdings BV, Berry Plastics Group Inc, Mondi Group, Tetra Pak International SA, Sealed Air Corporation, and Amcor PLC. However, a dynamic competitive environment is fostered by the presence of numerous smaller companies and a growing number of innovative startups.

Market dominance is significantly shaped by technological innovation, global reach, and product diversification strategies. Intense M&A activity characterizes the industry, with an estimated [Insert Precise Number] of deals recorded between 2019 and 2024. These mergers and acquisitions are primarily driven by the strategic goals of expanding product portfolios, accessing new markets, and enhancing technological capabilities. Regulatory frameworks, especially those concerning biodegradability standards and broader sustainability regulations, exert a considerable influence on market dynamics. Competition from substitute products, such as traditional petroleum-based plastics, remains a challenge. However, the burgeoning demand for eco-friendly packaging solutions, coupled with end-user preferences for sustainable and ethically sourced materials, creates significant growth opportunities for biopolymer packaging manufacturers.

Biopolymer Packaging Industry Industry Insights & Trends

The biopolymer packaging market has demonstrated substantial growth, driven by several interconnected factors. The rising consumer preference for sustainable and eco-conscious packaging is a primary catalyst. Growing environmental awareness and increasingly stringent government regulations targeting plastic waste are also major contributors to this upward trend. Technological advancements in biopolymer production, resulting in improved material properties and cost reductions, have significantly accelerated market penetration. Further fueling market expansion are rising disposable incomes in developing economies and the booming e-commerce sector, both of which significantly increase the overall demand for packaging materials. The increasing popularity of convenient and ready-to-eat food products, which necessitates robust packaging solutions, provides additional momentum for market growth. The global market is projected to experience considerable expansion, with a substantial increase in demand across various end-use segments. This strong growth trajectory is anticipated to continue throughout the forecast period, propelled by the confluence of environmental concerns and heightened consumer awareness.

Key Markets & Segments Leading Biopolymer Packaging Industry

The Biopolymer Packaging market demonstrates strong regional variations in growth rates. While specific regional data would be analyzed further within the report, initial data suggests that Asia-Pacific region, followed by Europe and North America, are leading the market growth, largely due to the significant growth in the food and beverage industry in Asia.

Material Type: The demand for biodegradable materials is experiencing exponential growth. This is fueled by increasing environmental awareness and the implementation of stringent regulations worldwide, restricting the use of non-biodegradable plastics. Non-biodegradable biopolymers continue to hold a substantial share due to their cost-effectiveness and established applications.

End-user Industry: The food and beverage sector remains the dominant end-use segment, followed closely by retail and healthcare industries. The growth in these segments is primarily driven by the rise in demand for convenient packaging, along with heightened environmental concerns across various supply chains.

Drivers for Key Regions:

- Asia-Pacific: Rapid economic growth, rising disposable incomes, and increasing demand for packaged food and beverages. Significant investment in infrastructure and manufacturing facilities also contribute to this region's dominance.

- Europe: Stringent environmental regulations, increasing consumer awareness of sustainability, and a strong focus on eco-friendly packaging solutions drive the growth of the Biopolymer Packaging market in this region.

- North America: A well-established food and beverage industry and rising consumer demand for eco-friendly alternatives are prominent factors that fuel the region’s market growth.

Biopolymer Packaging Industry Product Developments

Recent years have showcased significant advancements in biopolymer packaging technologies. Innovation efforts are focused on enhancing biodegradability, improving material strength and barrier properties, and lowering production costs. The development of compostable and recyclable biopolymer packaging is gaining considerable traction, directly addressing environmental concerns and satisfying consumer demand for sustainable products. This emphasis on sustainable solutions enhances the competitive advantage of manufacturers, aligning with the global push to reduce plastic waste and promote circular economy principles. Specific examples of these developments include [Add specific examples of recent product innovations, e.g., new materials, processes, or applications].

Challenges in the Biopolymer Packaging Industry Market

The biopolymer packaging industry confronts several key challenges. Higher production costs compared to conventional plastics hinder widespread adoption, particularly in price-sensitive markets. Supply chain complexities and inconsistencies in the availability of bio-based raw materials present significant obstacles. Furthermore, a lack of standardized biodegradability testing methods across different regions can create regulatory uncertainty and market fragmentation. The competitive pressure from established players in the traditional plastic packaging industry also poses a significant barrier to market penetration. These factors collectively impact market growth and necessitate innovative solutions and supportive policy interventions.

Forces Driving Biopolymer Packaging Industry Growth

Several key factors drive the growth of the biopolymer packaging industry. Technological advancements lead to improved biopolymer properties, making them more competitive compared to traditional plastics. Favorable government policies promoting sustainable packaging and reducing plastic waste incentivize the industry. Growing consumer awareness regarding environmental issues and the demand for eco-friendly alternatives are strong market drivers. Furthermore, collaborations between biopolymer manufacturers and packaging companies lead to innovative solutions. This combination of technological advancement and regulatory support significantly accelerates market growth.

Long-Term Growth Catalysts in the Biopolymer Packaging Industry

Long-term growth in the biopolymer packaging industry is fueled by continuous innovation in biopolymer materials, leading to enhanced properties and wider applications. Strategic partnerships among raw material suppliers, packaging companies, and waste management firms streamline the supply chain. Expanding into new markets and applications, particularly in developing economies, will unlock substantial growth potential. This concerted effort to improve the performance and accessibility of biopolymer packaging contributes to its long-term sustainability and market expansion.

Emerging Opportunities in Biopolymer Packaging Industry

The Biopolymer Packaging industry offers several emerging opportunities. The growing demand for sustainable and compostable packaging in various end-use sectors, including food and beverages, creates significant market potential. Technological advancements in bio-based materials, allowing for enhanced properties and functionality, offer further avenues for growth. Expanding into new geographic markets, particularly in developing economies with rising demand for packaged goods, presents significant business prospects. The increasing focus on circular economy models fosters the emergence of innovative recycling and waste management solutions, further enhancing market expansion.

Leading Players in the Biopolymer Packaging Industry Sector

- United Biopolymers SA

- Taghleef Industries Inc

- Sonoco Products Company

- Constantia Flexibles Group GmbH

- Clondalkin Group Holdings BV

- Berry Plastics Group Inc

- Mondi Group

- Tetra Pak International SA

- Sealed Air Corporation

- Amcor PLC

Key Milestones in Biopolymer Packaging Industry Industry

- 2020: Increased regulatory pressure on single-use plastics fueled heightened demand for biodegradable alternatives.

- 2022: Several key players announced substantial investments in biopolymer production facilities, expanding manufacturing capacity significantly. [Add specific examples of companies and investments]

- 2023: Launch of several innovative biopolymer packaging solutions with enhanced properties (e.g., improved barrier, strength, and compostability). [Add specific examples of launched products]

- 2024: Significant mergers and acquisitions within the industry resulted in the creation of larger, more integrated companies. [Add specific examples of mergers and acquisitions]

Strategic Outlook for Biopolymer Packaging Industry Market

The Biopolymer Packaging market holds substantial future potential, driven by a confluence of factors: growing environmental awareness, stringent regulations against plastic pollution, and continuous technological innovation. Strategic partnerships and collaborations will be crucial for streamlining the supply chain and reducing production costs. Focus on developing high-performance biopolymers with enhanced properties is essential for widespread adoption. By addressing the challenges and capitalizing on emerging opportunities, the biopolymer packaging industry is poised for robust growth in the coming years, presenting significant investment potential for stakeholders.

Biopolymer Packaging Industry Segmentation

-

1. Material Type

-

1.1. Non-biodegradable

- 1.1.1. PET

- 1.1.2. PA

- 1.1.3. PTT

- 1.1.4. Other Material Types

-

1.2. Biodegradability

- 1.2.1. PLA

- 1.2.2. Starch Blends

- 1.2.3. PBAT

- 1.2.4. Other Biodegradability Types

-

1.1. Non-biodegradable

-

2. End-user Industry

- 2.1. Food and Beverages

- 2.2. Retail

- 2.3. Healthcare

- 2.4. Personal Care/Homecare

- 2.5. Other End-user Industries

Biopolymer Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Biopolymer Packaging Industry Regional Market Share

Geographic Coverage of Biopolymer Packaging Industry

Biopolymer Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; The Growing Government Regulations for Bio-based Packaging; Increasing Awareness for Human Well Being and Eco-friendly Products

- 3.3. Market Restrains

- 3.3.1. ; Performance Issues with Bio-based Materials; High Cost of Bio-packaging Materials

- 3.4. Market Trends

- 3.4.1. Food and Beverages Industry is Expected to Witness a Significant Growth during the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Non-biodegradable

- 5.1.1.1. PET

- 5.1.1.2. PA

- 5.1.1.3. PTT

- 5.1.1.4. Other Material Types

- 5.1.2. Biodegradability

- 5.1.2.1. PLA

- 5.1.2.2. Starch Blends

- 5.1.2.3. PBAT

- 5.1.2.4. Other Biodegradability Types

- 5.1.1. Non-biodegradable

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food and Beverages

- 5.2.2. Retail

- 5.2.3. Healthcare

- 5.2.4. Personal Care/Homecare

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. North America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Non-biodegradable

- 6.1.1.1. PET

- 6.1.1.2. PA

- 6.1.1.3. PTT

- 6.1.1.4. Other Material Types

- 6.1.2. Biodegradability

- 6.1.2.1. PLA

- 6.1.2.2. Starch Blends

- 6.1.2.3. PBAT

- 6.1.2.4. Other Biodegradability Types

- 6.1.1. Non-biodegradable

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Food and Beverages

- 6.2.2. Retail

- 6.2.3. Healthcare

- 6.2.4. Personal Care/Homecare

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Europe Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Non-biodegradable

- 7.1.1.1. PET

- 7.1.1.2. PA

- 7.1.1.3. PTT

- 7.1.1.4. Other Material Types

- 7.1.2. Biodegradability

- 7.1.2.1. PLA

- 7.1.2.2. Starch Blends

- 7.1.2.3. PBAT

- 7.1.2.4. Other Biodegradability Types

- 7.1.1. Non-biodegradable

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Food and Beverages

- 7.2.2. Retail

- 7.2.3. Healthcare

- 7.2.4. Personal Care/Homecare

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Asia Pacific Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Non-biodegradable

- 8.1.1.1. PET

- 8.1.1.2. PA

- 8.1.1.3. PTT

- 8.1.1.4. Other Material Types

- 8.1.2. Biodegradability

- 8.1.2.1. PLA

- 8.1.2.2. Starch Blends

- 8.1.2.3. PBAT

- 8.1.2.4. Other Biodegradability Types

- 8.1.1. Non-biodegradable

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Food and Beverages

- 8.2.2. Retail

- 8.2.3. Healthcare

- 8.2.4. Personal Care/Homecare

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Latin America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Non-biodegradable

- 9.1.1.1. PET

- 9.1.1.2. PA

- 9.1.1.3. PTT

- 9.1.1.4. Other Material Types

- 9.1.2. Biodegradability

- 9.1.2.1. PLA

- 9.1.2.2. Starch Blends

- 9.1.2.3. PBAT

- 9.1.2.4. Other Biodegradability Types

- 9.1.1. Non-biodegradable

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Food and Beverages

- 9.2.2. Retail

- 9.2.3. Healthcare

- 9.2.4. Personal Care/Homecare

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Middle East and Africa Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Non-biodegradable

- 10.1.1.1. PET

- 10.1.1.2. PA

- 10.1.1.3. PTT

- 10.1.1.4. Other Material Types

- 10.1.2. Biodegradability

- 10.1.2.1. PLA

- 10.1.2.2. Starch Blends

- 10.1.2.3. PBAT

- 10.1.2.4. Other Biodegradability Types

- 10.1.1. Non-biodegradable

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Food and Beverages

- 10.2.2. Retail

- 10.2.3. Healthcare

- 10.2.4. Personal Care/Homecare

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. North America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Spain

- 12.1.5 Italy

- 12.1.6 Spain

- 12.1.7 Belgium

- 12.1.8 Netherland

- 12.1.9 Nordics

- 12.1.10 Rest of Europe

- 13. Asia Pacific Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 South Korea

- 13.1.5 Southeast Asia

- 13.1.6 Australia

- 13.1.7 Indonesia

- 13.1.8 Phillipes

- 13.1.9 Singapore

- 13.1.10 Thailandc

- 13.1.11 Rest of Asia Pacific

- 14. South America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 Brazil

- 14.1.2 Argentina

- 14.1.3 Peru

- 14.1.4 Chile

- 14.1.5 Colombia

- 14.1.6 Ecuador

- 14.1.7 Venezuela

- 14.1.8 Rest of South America

- 15. North America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 United States

- 15.1.2 Canada

- 15.1.3 Mexico

- 16. MEA Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1 United Arab Emirates

- 16.1.2 Saudi Arabia

- 16.1.3 South Africa

- 16.1.4 Rest of Middle East and Africa

- 17. Competitive Analysis

- 17.1. Global Market Share Analysis 2025

- 17.2. Company Profiles

- 17.2.1 United Biopolymers SA

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 Taghleef Industries Inc

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 Sonoco Products Company

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 Constantia Flexibles Group GmbH

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 Clondalkin Group Holdings BV

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.6 Berry Plastics Group Inc

- 17.2.6.1. Overview

- 17.2.6.2. Products

- 17.2.6.3. SWOT Analysis

- 17.2.6.4. Recent Developments

- 17.2.6.5. Financials (Based on Availability)

- 17.2.7 Mondi Group

- 17.2.7.1. Overview

- 17.2.7.2. Products

- 17.2.7.3. SWOT Analysis

- 17.2.7.4. Recent Developments

- 17.2.7.5. Financials (Based on Availability)

- 17.2.8 Tetra Pak International SA

- 17.2.8.1. Overview

- 17.2.8.2. Products

- 17.2.8.3. SWOT Analysis

- 17.2.8.4. Recent Developments

- 17.2.8.5. Financials (Based on Availability)

- 17.2.9 Sealed Air Corporation

- 17.2.9.1. Overview

- 17.2.9.2. Products

- 17.2.9.3. SWOT Analysis

- 17.2.9.4. Recent Developments

- 17.2.9.5. Financials (Based on Availability)

- 17.2.10 Amcor PLC*List Not Exhaustive

- 17.2.10.1. Overview

- 17.2.10.2. Products

- 17.2.10.3. SWOT Analysis

- 17.2.10.4. Recent Developments

- 17.2.10.5. Financials (Based on Availability)

- 17.2.1 United Biopolymers SA

List of Figures

- Figure 1: Global Biopolymer Packaging Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 3: North America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 4: Europe Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: Europe Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: South America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: MEA Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: MEA Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 15: North America Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 16: North America Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: North America Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: North America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: North America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Europe Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 21: Europe Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 22: Europe Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Europe Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Europe Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 27: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 33: Latin America Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 34: Latin America Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 35: Latin America Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 36: Latin America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Latin America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East and Africa Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 39: Middle East and Africa Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 40: Middle East and Africa Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 41: Middle East and Africa Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 42: Middle East and Africa Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 43: Middle East and Africa Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Biopolymer Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 2: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 3: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Biopolymer Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 6: United States Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Canada Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Mexico Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Germany Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: United Kingdom Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: France Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Spain Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Italy Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Spain Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Belgium Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Netherland Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Nordics Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Rest of Europe Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: China Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: India Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: South Korea Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Southeast Asia Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Indonesia Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Phillipes Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Singapore Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Thailandc Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 33: Brazil Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Argentina Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Peru Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Chile Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Colombia Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Ecuador Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Venezuela Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of South America Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: United States Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: Canada Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Mexico Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 46: United Arab Emirates Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 47: Saudi Arabia Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: South Africa Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 49: Rest of Middle East and Africa Biopolymer Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 51: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 52: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 53: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 54: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 55: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 57: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 58: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 59: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 60: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 61: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 62: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 63: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 64: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Biopolymer Packaging Industry?

The projected CAGR is approximately 12.60%.

2. Which companies are prominent players in the Biopolymer Packaging Industry?

Key companies in the market include United Biopolymers SA, Taghleef Industries Inc, Sonoco Products Company, Constantia Flexibles Group GmbH, Clondalkin Group Holdings BV, Berry Plastics Group Inc, Mondi Group, Tetra Pak International SA, Sealed Air Corporation, Amcor PLC*List Not Exhaustive.

3. What are the main segments of the Biopolymer Packaging Industry?

The market segments include Material Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; The Growing Government Regulations for Bio-based Packaging; Increasing Awareness for Human Well Being and Eco-friendly Products.

6. What are the notable trends driving market growth?

Food and Beverages Industry is Expected to Witness a Significant Growth during the Forecast Period.

7. Are there any restraints impacting market growth?

; Performance Issues with Bio-based Materials; High Cost of Bio-packaging Materials.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Biopolymer Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Biopolymer Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Biopolymer Packaging Industry?

To stay informed about further developments, trends, and reports in the Biopolymer Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence