Key Insights

The Poland automotive lubricants market, while exhibiting a moderate Compound Annual Growth Rate (CAGR) of 2.64%, presents a promising landscape for investors and industry players. Driven by a growing automotive sector, increasing vehicle ownership, and a rising demand for high-performance lubricants, the market is projected to experience steady expansion throughout the forecast period (2025-2033). Key market drivers include the increasing popularity of passenger vehicles, a robust commercial vehicle segment fueled by logistics and transportation growth, and a rising focus on extending vehicle lifespan through proper lubrication. Furthermore, stringent emission regulations are pushing the adoption of advanced lubricant technologies, particularly those formulated for fuel efficiency and environmental protection. While the market faces potential restraints such as economic fluctuations and price volatility in raw materials, the overall outlook remains positive, supported by ongoing investments in automotive manufacturing and the continued implementation of stricter vehicle maintenance standards. Major players like BP PLC (Castrol), ExxonMobil, and Shell, along with significant regional players like Lotos Oil and PKN ORLEN, are actively competing in this space, focusing on innovation and brand building to secure market share. The segmentation of the market likely includes passenger car motor oils, heavy-duty diesel engine oils, and specialty lubricants, each with its own growth trajectory and market dynamics. The historical period (2019-2024) likely saw variations in growth influenced by global economic conditions and specific industry developments within Poland.

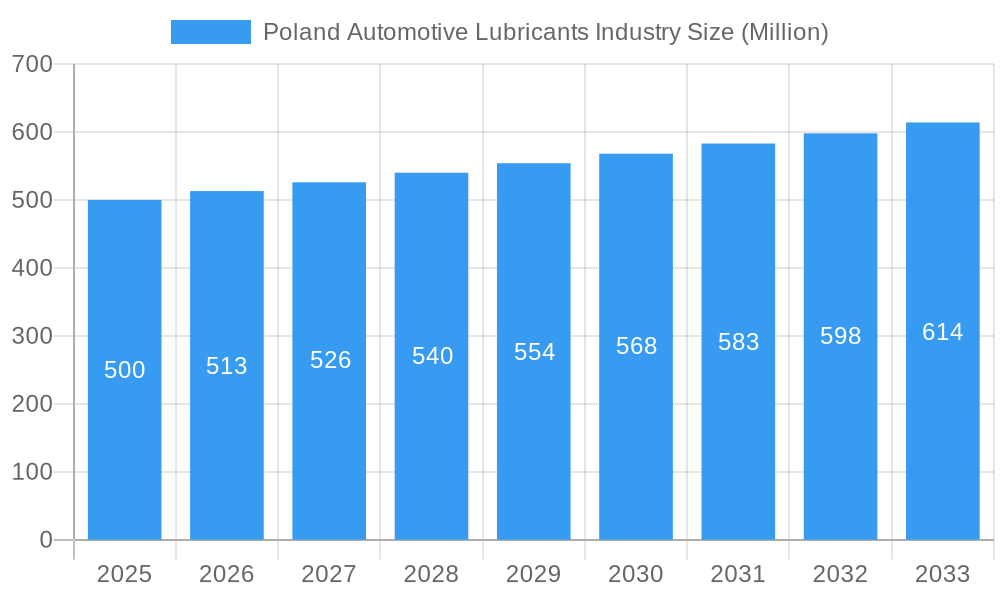

Poland Automotive Lubricants Industry Market Size (In Million)

Given a CAGR of 2.64% and a base year of 2025, we can reasonably assume a positive market trend. While the exact market size (XX million) is unavailable, we can project future market values based on the provided CAGR. For example, if we assume a 2025 market size of 500 million (a reasonable estimate based on similar markets), the 2026 market size would be approximately 513.2 million (500 million * 1.0264), and so on for subsequent years. This growth trajectory is largely influenced by the factors detailed above. Regional variations within Poland likely exist, reflecting differences in automotive density and economic activity across various provinces. Competition among established players and the potential emergence of new entrants adds another layer of complexity to the market dynamics, requiring ongoing monitoring of product innovation, market share shifts, and price competitiveness.

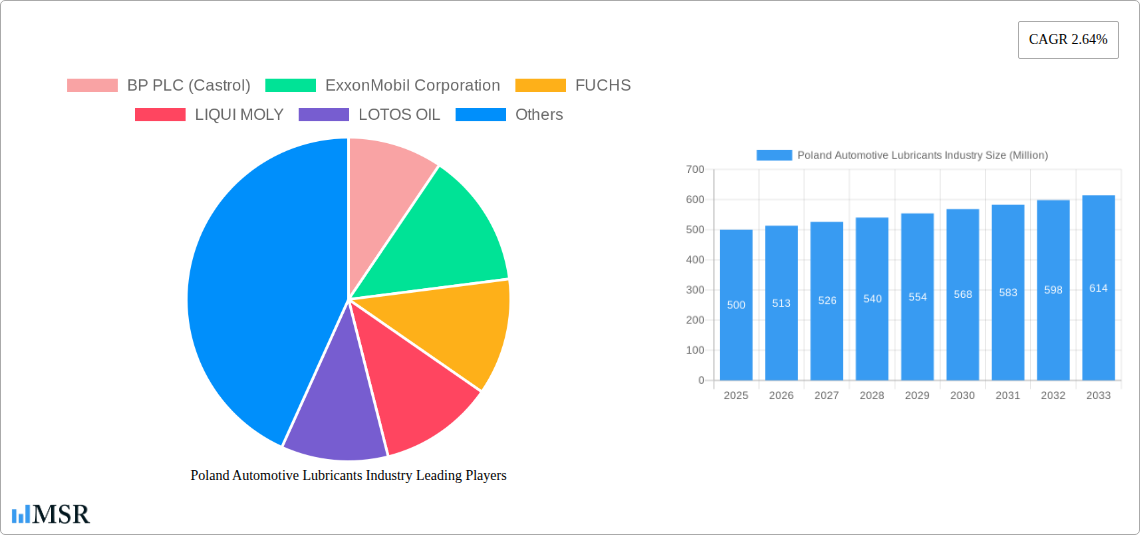

Poland Automotive Lubricants Industry Company Market Share

Poland Automotive Lubricants Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Poland automotive lubricants industry, covering market dynamics, key players, emerging trends, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers crucial insights for industry stakeholders, investors, and businesses operating within or seeking entry into this dynamic market. The report leverages extensive research and data analysis to deliver actionable intelligence. The Poland automotive lubricants market, valued at xx Million in 2024, is projected to reach xx Million by 2033, exhibiting a CAGR of xx%.

Poland Automotive Lubricants Industry Market Concentration & Dynamics

The Poland automotive lubricants market exhibits a moderately concentrated structure, with a handful of multinational corporations holding significant market share. Key players such as BP PLC (Castrol), ExxonMobil Corporation, and Royal Dutch Shell Plc compete fiercely, alongside regional players like LOTOS OIL and PKN ORLEN (ORLEN oil). The market share of these leading players collectively accounts for approximately xx%. Innovation in the sector is driven by the need to meet increasingly stringent emission regulations and evolving consumer preferences for higher-performing, eco-friendly lubricants.

The regulatory framework, largely aligned with EU standards, impacts product formulation and labeling. Substitute products, such as bio-based lubricants, are gaining traction, presenting both opportunities and challenges for traditional players. End-user trends toward longer vehicle lifespans and increased demand for specialized lubricants for diverse applications, like electric vehicles, further shape market dynamics. M&A activity in the sector has been relatively moderate in recent years, with approximately xx deals recorded during the historical period (2019-2024), primarily focused on smaller players and strategic partnerships.

Poland Automotive Lubricants Industry Industry Insights & Trends

The Poland automotive lubricants market is experiencing robust growth fueled by several key factors. The expanding automotive sector, particularly the increase in vehicle ownership and the rise of the commercial vehicle segment, drives demand for lubricants. Economic growth in Poland and increasing disposable incomes contribute to higher vehicle sales and maintenance activity. Technological advancements are significantly influencing the market. The introduction of advanced lubricant formulations, such as low-SAPS (sulfated ash, phosphorus, and sulfur) oils, cater to the demands of modern engine technologies and emission control systems. Consumer behavior is shifting towards a preference for high-quality, specialized lubricants that offer enhanced performance and extended drain intervals. The market is also witnessing a growing demand for eco-friendly, biodegradable lubricants reflecting the increased environmental consciousness of consumers and regulatory pressures. The market's growth trajectory reflects these trends, with a projected CAGR of xx% from 2025 to 2033, positioning Poland as a significant player in the Central European automotive lubricants market.

Key Markets & Segments Leading Poland Automotive Lubricants Industry

The Polish automotive lubricants market is largely driven by the passenger car segment, which accounts for the highest volume consumption. This dominance is attributed to the increasing number of passenger vehicles on the road, coupled with regular maintenance requirements. However, the commercial vehicle segment is exhibiting strong growth potential, driven by the expansion of logistics and transportation industries.

- Drivers of Passenger Car Segment Dominance:

- High vehicle ownership rates.

- Regular maintenance schedules.

- Growing demand for high-performance lubricants.

- Drivers of Commercial Vehicle Segment Growth:

- Expansion of logistics and transportation.

- Stringent emission regulations requiring specialized lubricants.

- Increased demand for heavy-duty engine oils.

The dominance of the passenger car segment is primarily attributable to the higher volume of vehicles on Polish roads compared to commercial vehicles. However, the increasing demand for heavy-duty vehicles for transportation and logistics signifies a growing market for specialized lubricants in the commercial vehicle sector. This presents an opportunity for players to cater to the evolving needs of this segment with tailored product offerings and solutions.

Poland Automotive Lubricants Industry Product Developments

Recent product developments in the Polish automotive lubricants market have focused on enhancing performance, extending drain intervals, and improving environmental compatibility. Formulations are increasingly tailored to meet the stringent emission standards and performance requirements of modern engines, including gasoline, diesel, and hybrid powertrains. The introduction of low-SAPS oils and synthetic-based lubricants reflects a push toward higher efficiency and reduced environmental impact. These advancements deliver competitive advantages to manufacturers and provide end-users with improved fuel economy, extended engine life, and reduced emissions.

Challenges in the Poland Automotive Lubricants Industry Market

The Polish automotive lubricants market faces several challenges. Fluctuations in crude oil prices directly impact raw material costs and lubricant pricing, affecting profitability. Intense competition among both domestic and international players creates pressure on pricing and margins. Stringent environmental regulations necessitate continuous investment in research and development to comply with evolving standards. Supply chain disruptions, particularly those stemming from geopolitical instability, can lead to shortages of essential raw materials. These factors, collectively, can impede market growth and profitability for businesses in this sector.

Forces Driving Poland Automotive Lubricants Industry Growth

Several factors contribute to the growth of the Polish automotive lubricants market. Strong economic growth and rising disposable incomes fuel higher vehicle sales and maintenance activity. The expansion of the automotive industry, including both passenger and commercial vehicles, necessitates increased lubricant consumption. Technological advancements in lubricant formulations, like low-SAPS oils and bio-based lubricants, enhance performance and address environmental concerns. Government initiatives aimed at improving infrastructure and supporting the automotive sector also contribute to market expansion. These factors collectively drive sustained growth in the sector.

Long-Term Growth Catalysts in the Poland Automotive Lubricants Industry

Long-term growth in the Polish automotive lubricants market will be driven by strategic partnerships between lubricant manufacturers and automotive OEMs. Innovation in lubricant technologies, focusing on electric vehicle fluids and sustainable bio-based alternatives, will play a crucial role. Expanding into new market segments, such as industrial applications, could unlock significant growth opportunities. Government support for green technologies and stricter emission regulations will further incentivize the adoption of advanced, environmentally friendly lubricants.

Emerging Opportunities in Poland Automotive Lubricants Industry

Emerging opportunities include the growing demand for specialized lubricants for electric vehicles (EVs) and hybrid vehicles. The increasing focus on sustainability is creating opportunities for bio-based and environmentally friendly lubricants. The expansion of the industrial sector, including manufacturing and construction, presents opportunities for specialized industrial lubricants. Developing digital solutions to enhance supply chain management and customer engagement can also unlock new growth avenues.

Leading Players in the Poland Automotive Lubricants Industry Sector

Key Milestones in Poland Automotive Lubricants Industry Industry

- June 2021: TotalEnergies and Stellantis group renewed their partnership, extending to Opel and Vauxhall, encompassing lubricant development and first-fill in Stellantis vehicles. This significantly boosted TotalEnergies' market presence and solidified its position as a key player in the automotive lubricants sector.

- October 2021: Valvoline and Cummins extended their collaboration for another five years, boosting Valvoline’s market share within the heavy-duty segment through Cummins' vast distribution network. This strengthened Valvoline's position in the commercial vehicle lubricant market.

- January 2022: ExxonMobil Corporation reorganized into three business lines, including ExxonMobil Product Solutions, streamlining its operations and potentially focusing resources on lubricant development and marketing. This restructuring could lead to increased competitiveness in the market.

Strategic Outlook for Poland Automotive Lubricants Industry Market

The future of the Polish automotive lubricants market appears promising, driven by sustained economic growth, technological advancements, and a growing awareness of environmental sustainability. Strategic opportunities exist in developing specialized lubricants for emerging vehicle technologies (EVs, hybrids) and in leveraging digital technologies to optimize supply chains and customer service. Companies that successfully adapt to the changing regulatory landscape, embrace technological innovation, and build strong partnerships will be well-positioned to capture significant market share and drive growth in this dynamic sector.

Poland Automotive Lubricants Industry Segmentation

-

1. Vehicle Type

- 1.1. Commercial Vehicles

- 1.2. Motorcycles

- 1.3. Passenger Vehicles

-

2. Product Type

- 2.1. Engine Oils

- 2.2. Greases

- 2.3. Hydraulic Fluids

- 2.4. Transmission & Gear Oils

Poland Automotive Lubricants Industry Segmentation By Geography

- 1. Poland

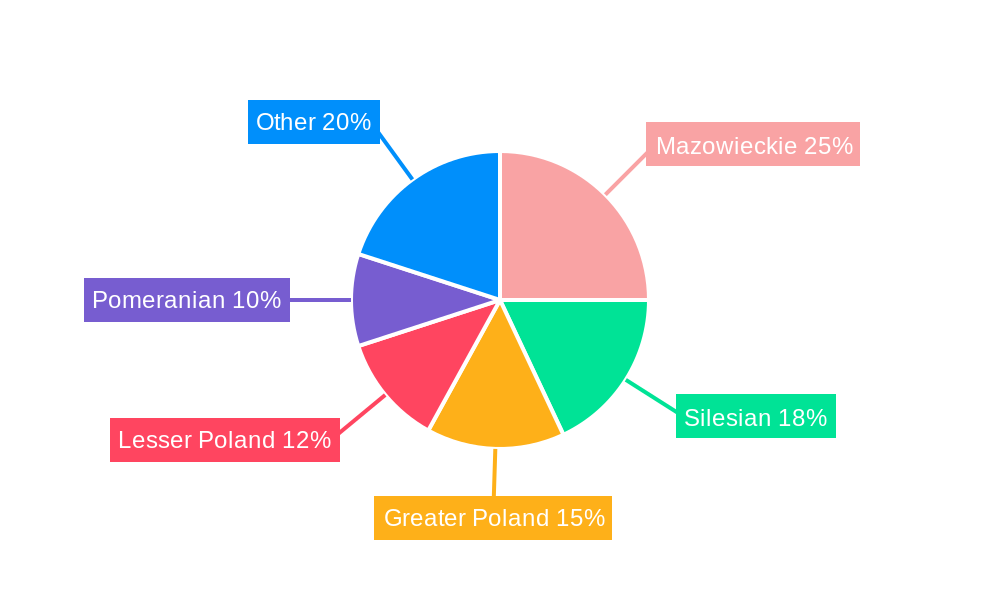

Poland Automotive Lubricants Industry Regional Market Share

Geographic Coverage of Poland Automotive Lubricants Industry

Poland Automotive Lubricants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Largest Segment By Vehicle Type

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Automotive Lubricants Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Commercial Vehicles

- 5.1.2. Motorcycles

- 5.1.3. Passenger Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Engine Oils

- 5.2.2. Greases

- 5.2.3. Hydraulic Fluids

- 5.2.4. Transmission & Gear Oils

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 BP PLC (Castrol)

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 ExxonMobil Corporation

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 FUCHS

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 LIQUI MOLY

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 LOTOS OIL

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Modex Oil

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Motul

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 PKN ORLEN (ORLEN oil)

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Royal Dutch Shell Plc

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 TotalEnergies

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Valvoline Inc

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 BP PLC (Castrol)

List of Figures

- Figure 1: Poland Automotive Lubricants Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Poland Automotive Lubricants Industry Share (%) by Company 2025

List of Tables

- Table 1: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 2: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Vehicle Type 2020 & 2033

- Table 3: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 4: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Vehicle Type 2020 & 2033

- Table 6: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 7: Poland Automotive Lubricants Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Automotive Lubricants Industry?

The projected CAGR is approximately 2.64%.

2. Which companies are prominent players in the Poland Automotive Lubricants Industry?

Key companies in the market include BP PLC (Castrol), ExxonMobil Corporation, FUCHS, LIQUI MOLY, LOTOS OIL, Modex Oil, Motul, PKN ORLEN (ORLEN oil), Royal Dutch Shell Plc, TotalEnergies, Valvoline Inc.

3. What are the main segments of the Poland Automotive Lubricants Industry?

The market segments include Vehicle Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Largest Segment By Vehicle Type : Passenger Vehicles.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.October 2021: Valvoline and Cummins extended their long-standing marketing and technology collaboration agreement for another five years. Cummins will endorse and promote Valvoline's Premium Blue engine oil for its heavy-duty diesel engines and generators and will distribute Valvoline products through its global distribution networks.June 2021: TotalEnergies and Stellantis group renewed their partnership for cooperation across different segments. Along with the renewal of partnerships with Peugeot, Citroën, and DS Automobiles, the new collaboration extends to Opel, and Vauxhall as well. This partnership includes the development and innovation of lubricants, first-fill in Stellantis group vehicles, recommendation of Quartz lubricants, and shared usage of charging stations operated by TotalEnergies, among others.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Automotive Lubricants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Automotive Lubricants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Automotive Lubricants Industry?

To stay informed about further developments, trends, and reports in the Poland Automotive Lubricants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence