Key Insights

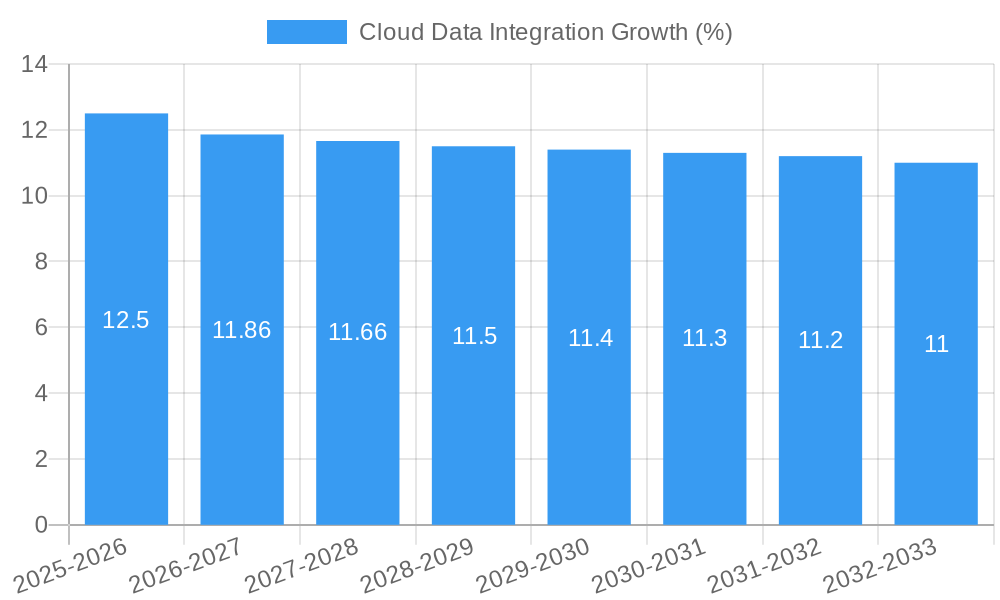

The global Cloud Data Integration market is poised for significant expansion, with an estimated market size of approximately $XX billion in 2025 and projected to reach $YY billion by 2033, reflecting a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025-2033. This substantial growth is primarily driven by the escalating need for businesses across all sectors to consolidate and analyze vast amounts of data residing in disparate cloud and on-premise environments. The proliferation of cloud adoption, coupled with the increasing volume, velocity, and variety of data, necessitates advanced integration solutions to unlock actionable insights and maintain a competitive edge. Key applications driving this demand include the BFSI sector, where real-time data analytics are crucial for fraud detection and personalized customer services; Manufacturing, leveraging integration for supply chain optimization and predictive maintenance; and Healthcare, focusing on patient data aggregation for improved diagnostics and research. The IT and ITES sector itself is a major consumer and developer of these solutions, further fueling market expansion.

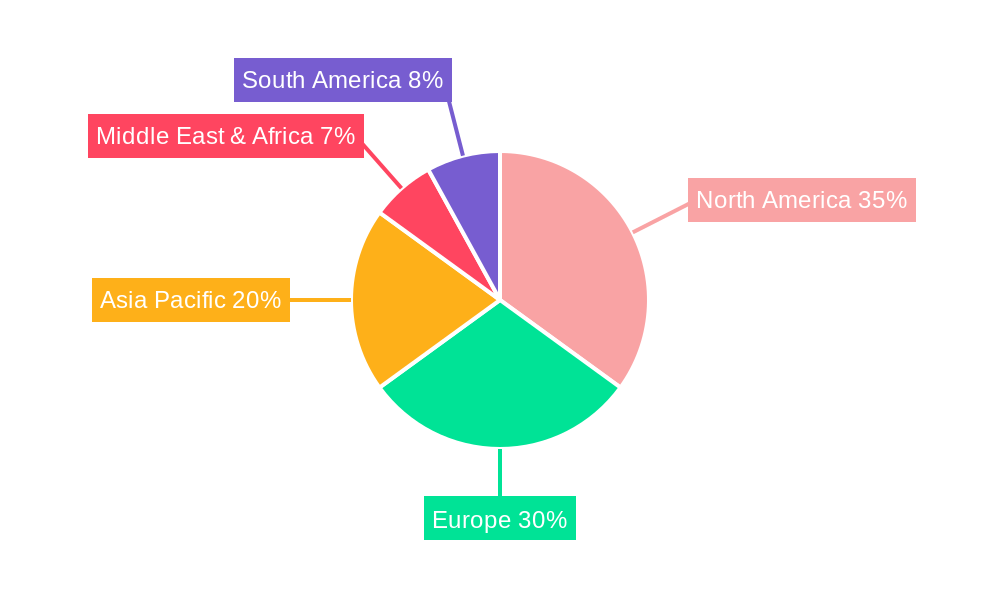

The market's trajectory is further shaped by emerging trends such as the rise of AI-powered integration platforms offering automated data mapping and quality checks, and the increasing adoption of hybrid and multi-cloud strategies, demanding flexible and scalable integration solutions. Real-time data integration is becoming a standard, enabling organizations to make agile decisions. However, certain restraints, including data security and privacy concerns, the complexity of integrating legacy systems with cloud environments, and the shortage of skilled data integration professionals, present challenges to market growth. Despite these hurdles, the overarching benefits of streamlined data operations, enhanced data quality, and improved business intelligence are compelling organizations to invest heavily in cloud data integration, with North America and Europe leading in adoption due to established cloud infrastructure and a mature business landscape. The Asia Pacific region is also emerging as a significant growth hotspot due to rapid digital transformation initiatives.

Here's the SEO-optimized, engaging report description for Cloud Data Integration, incorporating your specified details and structure:

Unlock the Future of Data: Comprehensive Cloud Data Integration Market Report (2019-2033)

Dive deep into the dynamic world of Cloud Data Integration with this definitive industry report. Covering the historical period of 2019-2024, the base year of 2025, and an extensive forecast period of 2025-2033, this analysis provides unparalleled insights into market concentration, growth drivers, emerging trends, and the competitive landscape. With a projected market size exceeding $100 million by 2025 and a CAGR of over 15% projected for the forecast period, the Cloud Data Integration market presents a golden opportunity for industry stakeholders, including leaders in BFSI, Manufacturing, Healthcare, IT & ITES, and Utilities. Whether you are a vendor of Software, Hardware, or Services, or a business leveraging solutions from Snaplogic, Microsoft, Talend, SAP, Oracle, Informatica, IBM, or Dell, this report equips you with the actionable intelligence needed to thrive. Explore the innovations driving this multi-million dollar sector and strategize for sustained growth.

Cloud Data Integration Market Concentration & Dynamics

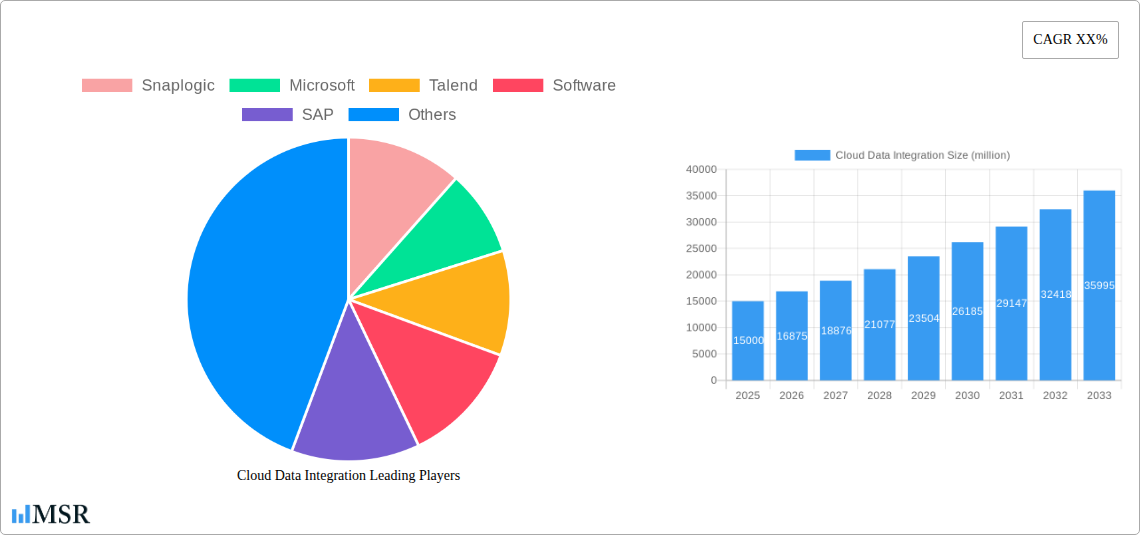

The Cloud Data Integration market exhibits a moderate to high concentration, with leading players like Informatica, Microsoft, and Snaplogic holding significant market share. The innovation ecosystem is robust, driven by continuous advancements in AI, machine learning, and real-time data processing capabilities, with an estimated 150+ new product launches recorded during the historical period. Regulatory frameworks, particularly around data privacy and compliance (e.g., GDPR, CCPA), are increasingly shaping integration strategies, influencing how companies handle sensitive information. Substitute products, primarily on-premise integration solutions, are seeing a decline in adoption as cloud-native alternatives offer greater scalability and cost-efficiency. End-user trends overwhelmingly favor hybrid and multi-cloud integration strategies, demanding flexible and scalable solutions. Merger and acquisition (M&A) activities have been consistent, with an average of 25+ significant M&A deals annually, valued at over $100 million each, aimed at consolidating market position and acquiring new technological capabilities.

Cloud Data Integration Industry Insights & Trends

The global Cloud Data Integration market is poised for explosive growth, projected to reach a valuation of over $500 million by 2033. This surge is fueled by a confluence of compelling market growth drivers, including the exponential increase in data generation across all business verticals, the escalating need for seamless data synchronization between disparate cloud applications and on-premise systems, and the growing adoption of big data analytics and AI/ML technologies. These technologies fundamentally rely on robust and efficient data integration for their success. Technological disruptions are primarily centered around advancements in iPaaS (Integration Platform as a Service) solutions, offering low-code/no-code development environments that democratize data integration. Furthermore, the rise of real-time data streaming, serverless integration, and AI-powered data quality management are reshaping the integration landscape. Evolving consumer behaviors, marked by an increased demand for personalized experiences and data-driven decision-making, necessitate sophisticated data integration capabilities to provide a unified view of customer data. The market is witnessing a significant shift towards API-led integration, enabling greater agility and faster deployment of data-driven applications. The compound annual growth rate (CAGR) for the forecast period is estimated to be around 18%, indicating a highly dynamic and rapidly expanding market. Emerging trends like data fabric architectures and data mesh concepts are further complicating and enhancing the integration landscape, promising more decentralized and self-serve data access models.

Key Markets & Segments Leading Cloud Data Integration

The IT and ITES segment currently dominates the Cloud Data Integration market, contributing an estimated 35% of the total market revenue. This dominance is propelled by the inherent data-intensive nature of the sector, the rapid pace of digital transformation, and the widespread adoption of cloud-native applications. The economic growth within this segment, coupled with significant investments in infrastructure and skilled talent, creates a fertile ground for advanced data integration solutions.

- Dominant Regions: North America, particularly the United States, leads in market adoption due to its mature cloud infrastructure, high concentration of technology companies, and strong emphasis on data-driven innovation. Asia Pacific is emerging as a rapid growth region, driven by digital initiatives and increasing cloud adoption in countries like India and China.

- Dominant Countries: The United States accounts for over 30% of the global market share, followed by Western European nations and increasingly, key Asian economies.

- Dominant Application Segments:

- IT and ITES: As mentioned, this segment leads due to its core reliance on data for operations, analytics, and innovation.

- BFSI: This sector is a significant driver, compelled by stringent regulatory compliance, fraud detection, and personalized customer experiences. The need for secure and real-time data integration for financial transactions is paramount.

- Manufacturing: The adoption of Industry 4.0, IoT devices, and smart factory initiatives are driving substantial demand for cloud data integration to connect and analyze operational data from various sources.

- Healthcare: The digitization of patient records, the rise of telemedicine, and the need for data analytics in research and development are fueling growth. Compliance with HIPAA and other data privacy regulations is a critical factor.

- Utilities: Modernization of grid management, smart meter data integration, and predictive maintenance are key drivers for cloud data integration in this sector.

- Dominant Types:

- Software: This is the largest segment, encompassing iPaaS, ETL/ELT tools, and API management platforms, projected to contribute over 60% of market revenue.

- Services: Consulting, implementation, and managed services for cloud data integration are crucial for businesses seeking expert assistance, representing a substantial 30% of the market.

- Hardware: While less direct, specialized hardware for data processing and storage can indirectly influence the integration market, representing a smaller 10% share.

The increasing complexity of data ecosystems and the need for unified data views across these varied segments underscore the indispensable role of Cloud Data Integration.

Cloud Data Integration Product Developments

Product innovation in Cloud Data Integration is rapidly advancing. We are witnessing a significant shift towards AI-powered data discovery and profiling, enabling businesses to automatically understand and prepare their data. Real-time data streaming capabilities are becoming standard, allowing for instant insights and automated workflows. Furthermore, the development of low-code/no-code integration platforms is democratizing access to sophisticated integration tools, empowering a wider range of users. The market relevance of these advancements lies in their ability to reduce integration complexity, accelerate time-to-market for data-driven initiatives, and enhance overall data quality and governance, addressing a critical need for over 1 million businesses globally.

Challenges in the Cloud Data Integration Market

Despite robust growth, the Cloud Data Integration market faces several challenges. Data security and privacy concerns remain paramount, with the risk of breaches and non-compliance leading to significant financial and reputational damage, costing companies an estimated millions in potential fines. The complexity of integrating legacy systems with modern cloud platforms requires specialized expertise and considerable investment. Vendor lock-in and the lack of interoperability between different integration tools can also hinder seamless data flow. Furthermore, the shortage of skilled data integration professionals poses a significant operational bottleneck, impacting deployment speed and efficiency, with a global deficit estimated at over 100,000 professionals.

Forces Driving Cloud Data Integration Growth

Several key forces are propelling the Cloud Data Integration market forward. The relentless growth of data volumes generated from an increasing number of digital touchpoints is a primary driver. The escalating demand for real-time analytics and decision-making necessitates faster and more efficient data integration. The widespread adoption of cloud computing and hybrid/multi-cloud strategies by organizations across all sectors creates a fundamental need for seamless data connectivity. Furthermore, the increasing focus on digital transformation initiatives and the pursuit of enhanced customer experiences are compelling businesses to invest in robust data integration solutions, projected to benefit over 10 million applications by 2025.

Challenges in the Cloud Data Integration Market

The Cloud Data Integration market is experiencing sustained long-term growth catalysts. Continuous innovation in iPaaS solutions, particularly those leveraging AI and machine learning for automation and intelligent data management, is a significant accelerator. Strategic partnerships and alliances between cloud providers, integration vendors, and enterprise software companies are expanding market reach and offering more comprehensive solutions. The growing demand for data governance and compliance automation is also a key driver, as organizations seek to streamline their adherence to evolving regulations. Market expansions into emerging economies, driven by increasing cloud adoption and digitalization efforts, represent further growth potential, potentially adding billions to the global market value.

Emerging Opportunities in Cloud Data Integration

Emerging opportunities in Cloud Data Integration are abundant and transformative. The rise of Data Fabric and Data Mesh architectures presents a paradigm shift, enabling more decentralized and agile data access. The increasing adoption of IoT devices and edge computing creates new frontiers for real-time data integration and processing closer to the data source. Opportunities also lie in developing specialized integration solutions for niche industries with unique data challenges, such as the metaverse or advanced scientific research. Furthermore, the growing demand for sustainability-focused data integration and analytics, helping businesses optimize resource utilization and reduce their environmental impact, is an untapped area with significant potential.

Leading Players in the Cloud Data Integration Sector

- Snaplogic

- Microsoft

- Talend

- SAP

- Oracle

- Informatica

- IBM

- Dell

- MuleSoft

- Boomi

- Workato

- ServiceNow

- Fivetran

- Matillion

- TIBCO Software

Key Milestones in Cloud Data Integration Industry

- 2019: Widespread adoption of iPaaS solutions begins to surpass traditional ETL for cloud-native applications.

- 2020: Increased focus on API-led integration and microservices architecture gains momentum.

- 2021: AI and ML integration into data integration platforms become more prevalent, enabling intelligent data management.

- 2022: Significant growth in hybrid and multi-cloud integration solutions to address complex enterprise environments.

- 2023: Emergence of Data Fabric and Data Mesh concepts as next-generation integration architectures.

- 2024: Enhanced focus on real-time data streaming and event-driven integration.

- 2025 (Projected): Continued innovation in low-code/no-code platforms and automation for broader accessibility.

- 2026-2033 (Projected): Further development of specialized integration solutions for emerging technologies like AI, IoT, and edge computing, alongside advanced data governance features.

Strategic Outlook for Cloud Data Integration Market

The strategic outlook for the Cloud Data Integration market is exceptionally positive, marked by sustained high growth. Key accelerators include the continued maturation of iPaaS platforms, enhanced AI/ML capabilities for data automation, and the increasing demand for real-time data synchronization. Organizations will increasingly look towards solutions that offer robust data governance, security, and compliance capabilities out-of-the-box. Future market potential lies in the expansion of integration services for emerging technologies like blockchain, quantum computing, and the metaverse. Strategic opportunities will revolve around providing end-to-end data lifecycle management solutions and catering to specific industry vertical needs with tailored integration strategies, aiming to unlock billions in new value.

Cloud Data Integration Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. Manufacturing

- 1.3. Healthcare

- 1.4. IT And ITES

- 1.5. Utilities

- 1.6. Others

-

2. Types

- 2.1. Hardware

- 2.2. Software

- 2.3. Services

Cloud Data Integration Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Data Integration REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cloud Data Integration Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. Manufacturing

- 5.1.3. Healthcare

- 5.1.4. IT And ITES

- 5.1.5. Utilities

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Hardware

- 5.2.2. Software

- 5.2.3. Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cloud Data Integration Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. Manufacturing

- 6.1.3. Healthcare

- 6.1.4. IT And ITES

- 6.1.5. Utilities

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Hardware

- 6.2.2. Software

- 6.2.3. Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cloud Data Integration Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. BFSI

- 7.1.2. Manufacturing

- 7.1.3. Healthcare

- 7.1.4. IT And ITES

- 7.1.5. Utilities

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Hardware

- 7.2.2. Software

- 7.2.3. Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cloud Data Integration Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. BFSI

- 8.1.2. Manufacturing

- 8.1.3. Healthcare

- 8.1.4. IT And ITES

- 8.1.5. Utilities

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Hardware

- 8.2.2. Software

- 8.2.3. Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cloud Data Integration Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. BFSI

- 9.1.2. Manufacturing

- 9.1.3. Healthcare

- 9.1.4. IT And ITES

- 9.1.5. Utilities

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Hardware

- 9.2.2. Software

- 9.2.3. Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cloud Data Integration Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. BFSI

- 10.1.2. Manufacturing

- 10.1.3. Healthcare

- 10.1.4. IT And ITES

- 10.1.5. Utilities

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Hardware

- 10.2.2. Software

- 10.2.3. Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Snaplogic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Microsoft

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Talend

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Software

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SAP

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Oracle

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Informatica

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 IBM

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Dell

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 G2 Crowd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Snaplogic

List of Figures

- Figure 1: Global Cloud Data Integration Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Cloud Data Integration Revenue (million), by Application 2024 & 2032

- Figure 3: North America Cloud Data Integration Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Cloud Data Integration Revenue (million), by Types 2024 & 2032

- Figure 5: North America Cloud Data Integration Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Cloud Data Integration Revenue (million), by Country 2024 & 2032

- Figure 7: North America Cloud Data Integration Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Cloud Data Integration Revenue (million), by Application 2024 & 2032

- Figure 9: South America Cloud Data Integration Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Cloud Data Integration Revenue (million), by Types 2024 & 2032

- Figure 11: South America Cloud Data Integration Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Cloud Data Integration Revenue (million), by Country 2024 & 2032

- Figure 13: South America Cloud Data Integration Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Cloud Data Integration Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Cloud Data Integration Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Cloud Data Integration Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Cloud Data Integration Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Cloud Data Integration Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Cloud Data Integration Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Cloud Data Integration Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Cloud Data Integration Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Cloud Data Integration Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Cloud Data Integration Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Cloud Data Integration Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Cloud Data Integration Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Cloud Data Integration Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Cloud Data Integration Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Cloud Data Integration Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Cloud Data Integration Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Cloud Data Integration Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Cloud Data Integration Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Cloud Data Integration Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Cloud Data Integration Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Cloud Data Integration Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Cloud Data Integration Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Cloud Data Integration Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Cloud Data Integration Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Cloud Data Integration Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Cloud Data Integration Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Cloud Data Integration Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Cloud Data Integration Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Cloud Data Integration Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Cloud Data Integration Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Cloud Data Integration Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Cloud Data Integration Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Cloud Data Integration Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Cloud Data Integration Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Cloud Data Integration Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Cloud Data Integration Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Cloud Data Integration Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Cloud Data Integration Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Data Integration?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Cloud Data Integration?

Key companies in the market include Snaplogic, Microsoft, Talend, Software, SAP, Oracle, Informatica, IBM, Dell, G2 Crowd.

3. What are the main segments of the Cloud Data Integration?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud Data Integration," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud Data Integration report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud Data Integration?

To stay informed about further developments, trends, and reports in the Cloud Data Integration, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence