Key Insights

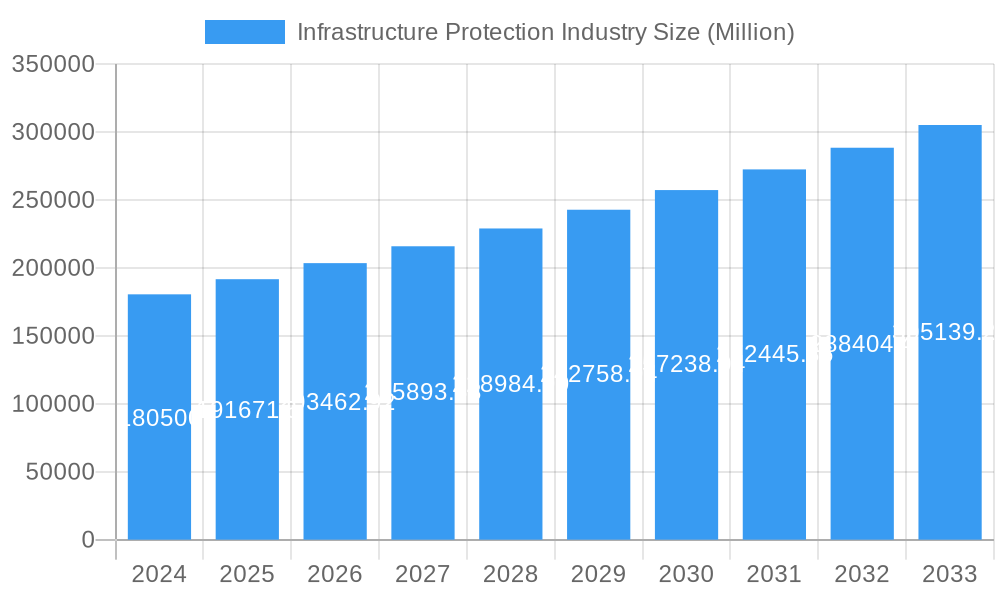

The global Infrastructure Protection market is projected for significant expansion, expected to reach $151.8 billion by 2025, with a robust CAGR of 4.4% through 2033. This growth is propelled by escalating physical and cyber threats targeting critical sectors including BFSI, Public Infrastructure & Transportation, Energy and Power, and IT & Telecom. Advancements in AI, IoT, and cloud computing are enhancing surveillance, threat detection, and response capabilities. The adoption of integrated security solutions, encompassing risk management, design, integration, consultation, managed services, and maintenance, highlights a comprehensive approach to asset protection. Emerging economies, particularly in the Asia Pacific, are poised for substantial growth driven by urbanization and infrastructure development.

Infrastructure Protection Industry Market Size (In Billion)

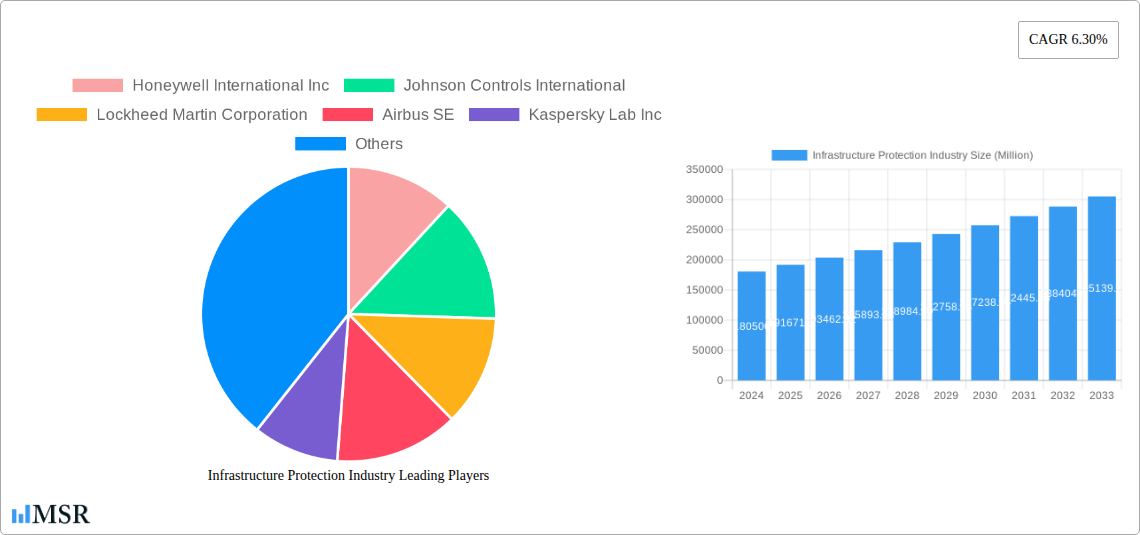

Despite positive growth, challenges include high initial investment costs for advanced security systems and the constant evolution of threat vectors. A global shortage of skilled cybersecurity professionals also poses a hurdle. However, increasing regulatory compliance and a greater awareness of the severe consequences of infrastructure breaches are driving security prioritization. Key industry players like Honeywell International Inc., Johnson Controls International, and Lockheed Martin Corporation are leading the market with diverse solutions. The trend favors proactive security measures, predictive analytics, and resilient infrastructure design to ensure operational continuity and national security.

Infrastructure Protection Industry Company Market Share

Report Overview:

This comprehensive analysis delves into the Infrastructure Protection industry, offering critical intelligence on cybersecurity solutions, physical security systems, and critical infrastructure defense. Explore market dynamics, growth drivers, and emerging trends impacting vital asset safeguarding across sectors like BFSI, Energy and Power, Public Infrastructure & Transportation, and IT & Telecom. Gain actionable insights into risk management, design and integration, and managed services. This report identifies key players such as Honeywell International Inc., Johnson Controls International, Lockheed Martin Corporation, Airbus SE, Kaspersky Lab Inc., General Dynamics, Rolta India Limited, Northrop Grumman Corporation, SCADAfence, BAE Systems plc, Waterfall Security Solutions, and McAfee Corp, detailing their strategic initiatives and innovations. Understand market concentration, regulatory landscapes, and the impact of technological advancements on this expanding sector.

Study Period: 2019–2033 Base Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

Infrastructure Protection Industry Market Concentration & Dynamics

The Infrastructure Protection Industry is characterized by a dynamic and evolving market concentration. While a few dominant players, including Honeywell International Inc, Johnson Controls International, and Lockheed Martin Corporation, hold significant market share, the landscape is increasingly populated by specialized firms focusing on niche areas like SCADAfence for industrial cybersecurity and Waterfall Security Solutions for operational technology. The innovation ecosystem thrives on a blend of established defense contractors and agile cybersecurity innovators, fostering continuous development in risk management services and advanced designing, integration, and consultation. Regulatory frameworks, particularly concerning public infrastructure & transportation and energy and power sectors, are tightening, mandating higher levels of security and compliance. Substitute products, such as advanced analytics replacing traditional manual surveillance, are emerging but are often integrated rather than pure replacements. End-user trends highlight a growing demand for holistic security strategies encompassing both physical and cybersecurity solutions. Merger and acquisition (M&A) activities are robust, with an estimated XX M&A deals in the historical period (2019-2024) indicating consolidation and strategic expansion, as seen with Johnson Controls' acquisition of Tempered Networks.

Infrastructure Protection Industry Industry Insights & Trends

The Infrastructure Protection Industry is experiencing robust growth, driven by a confluence of escalating threats and the increasing digitization of critical assets. The global market size is projected to reach approximately $XXX Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX.X% during the forecast period (2025–2033). A primary growth driver is the escalating sophistication and frequency of cyberattacks targeting critical infrastructure, including the BFSI, Energy and Power, and Public Infrastructure & Transportation sectors. The proliferation of the Internet of Things (IoT) and Industrial Internet of Things (IIoT) devices, while enhancing operational efficiency, also expands the attack surface, necessitating advanced cybersecurity solutions and managed services. Technological disruptions, such as the adoption of AI-powered threat detection, blockchain for secure data management, and advanced analytics for predictive security, are transforming protective measures. Evolving consumer behaviors, particularly the demand for seamless and integrated security experiences, are pushing providers to offer comprehensive protection across physical and digital domains. The integration of physical security with IT security is becoming paramount, with companies like Honeywell International Inc and Johnson Controls International leading this convergence. The growing emphasis on zero-trust architectures, as exemplified by Johnson Controls' acquisition of Tempered Networks, underscores a shift towards more granular and resilient security postures. Furthermore, government initiatives and investments in national security and critical infrastructure resilience are significantly bolstering market expansion. The growing need for effective Maintenance & Support services to ensure the continuous operational integrity of protection systems also contributes to market growth.

Key Markets & Segments Leading Infrastructure Protection Industry

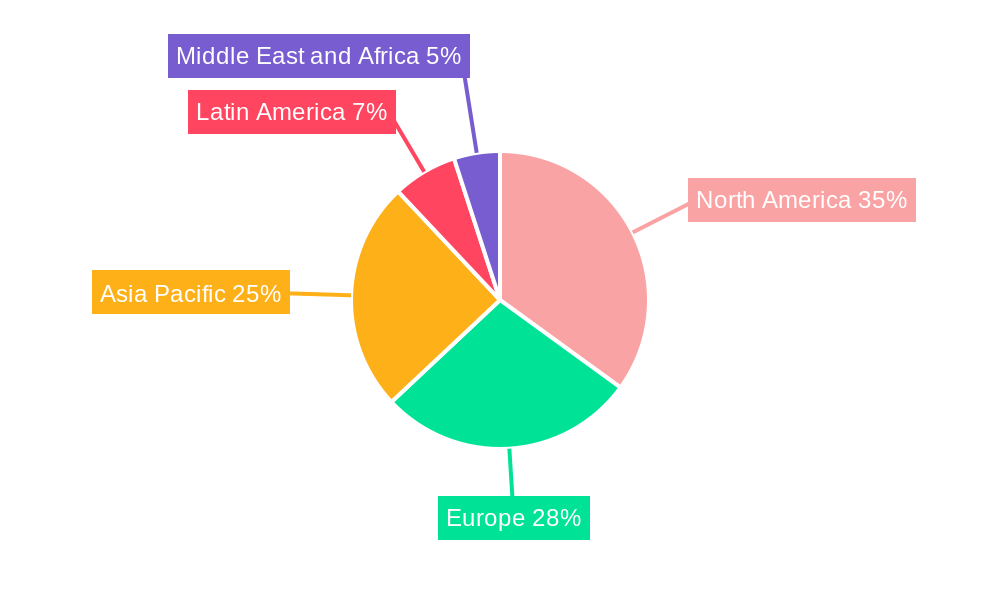

Several regions and segments are demonstrating significant leadership within the Infrastructure Protection Industry. North America and Europe currently represent the dominant geographic markets, driven by substantial government investment in national security, stringent regulatory compliance, and the high concentration of critical infrastructure.

Dominant Services Segments:

- Designing, Integration, and Consultation: This segment is crucial for developing bespoke security architectures tailored to the unique needs of diverse critical sectors like Energy and Power and Public Infrastructure & Transportation. Economic growth and ongoing infrastructure development projects in these regions necessitate expert design and seamless integration of advanced security systems.

- Managed Service: The increasing complexity of threat landscapes and the shortage of skilled cybersecurity professionals are driving the demand for managed services. Organizations are outsourcing the monitoring, management, and maintenance of their security infrastructure to specialized providers, ensuring 24/7 protection.

- Maintenance & Support: The long lifecycle and critical nature of infrastructure assets underscore the importance of reliable Maintenance & Support services. Ensuring the operational readiness and efficacy of security systems is paramount, especially in sectors prone to physical and cyber threats.

Dominant Verticals:

- Public Infrastructure & Transportation: This vertical is experiencing rapid growth due to heightened concerns over terrorism, cyberattacks on transportation networks (airports, rail, ports), and the need to secure smart city initiatives. Government mandates and significant infrastructure upgrade projects are key drivers.

- Energy and Power: The energy sector, including oil and gas, utilities, and renewable energy sources, is a prime target for malicious actors due to its foundational role in national economies. The increasing adoption of smart grids and SCADA systems further amplifies the need for robust cybersecurity solutions and operational technology protection.

- BFSI (Banking, Financial Services, and Insurance): This sector faces constant threats from financial fraud, data breaches, and cyberattacks aimed at disrupting financial markets. Stringent regulatory requirements and the need to protect sensitive customer data make it a leading adopter of comprehensive infrastructure protection.

- IT & Telecom: The backbone of modern economies, the IT and Telecom sector is under perpetual threat from data breaches, denial-of-service attacks, and espionage. The expanding digital footprint and reliance on cloud infrastructure necessitate advanced security measures.

The increasing global interconnectedness and the rise of sophisticated threat actors are creating demand across all sectors, but the sheer criticality and vulnerability of public infrastructure and energy resources make them focal points for protection strategies.

Infrastructure Protection Industry Product Developments

Product innovations in the Infrastructure Protection Industry are rapidly advancing, focusing on proactive threat detection and automated response. Companies are developing AI-powered surveillance systems that can identify anomalous behavior in real-time, advanced encryption technologies for securing sensitive data transmission, and hardened cybersecurity platforms designed to withstand sophisticated attacks. Solutions like those offered by SCADAfence are specifically targeting the protection of industrial control systems, while Waterfall Security Solutions specializes in secure gateways for operational technology environments. The market is seeing a surge in integrated solutions that combine physical and cybersecurity elements, offering a unified approach to asset protection. These developments are crucial for maintaining the integrity of critical infrastructure against an ever-evolving threat landscape.

Challenges in the Infrastructure Protection Industry Market

The Infrastructure Protection Industry faces several significant challenges. Regulatory hurdles, particularly navigating disparate compliance requirements across different jurisdictions and sectors, can be complex and costly to manage. Supply chain issues, including the sourcing of specialized hardware and the dependency on a limited number of manufacturers for critical components, can lead to delays and increased costs. Competitive pressures are intense, with a constant need for innovation to stay ahead of evolving threats, often requiring substantial R&D investments. Furthermore, the skills gap in cybersecurity expertise remains a persistent challenge, impacting the ability of organizations to effectively deploy and manage advanced protection systems. The estimated cost of security breaches due to these challenges could run into Millions of dollars annually for affected entities.

Forces Driving Infrastructure Protection Industry Growth

The Infrastructure Protection Industry's growth is propelled by several key forces. The escalating threat landscape, characterized by increasingly sophisticated and state-sponsored cyberattacks targeting critical national infrastructure, is a primary driver. Growing global investment in modernization and expansion of public utilities, transportation networks, and defense systems necessitates robust security solutions. Stringent government regulations and mandates for securing critical assets, particularly in sectors like energy and finance, are compelling organizations to enhance their protection measures. The rapid adoption of digital technologies, including IoT and AI, across all industries creates new vulnerabilities that demand advanced cybersecurity and physical security integration. Finally, the increasing awareness among businesses and governments regarding the potential catastrophic consequences of infrastructure compromise fuels proactive investment in protection.

Challenges in the Infrastructure Protection Industry Market

Long-term growth catalysts in the Infrastructure Protection Industry are deeply rooted in continuous innovation and strategic market expansion. The development and adoption of next-generation technologies, such as quantum-resistant cryptography and advanced AI for anomaly detection, will be crucial. Strategic partnerships and collaborations between cybersecurity firms, defense contractors, and technology providers are fostering more comprehensive and integrated solutions. Expanding into emerging markets with developing critical infrastructure presents significant growth opportunities. The trend towards outsourcing security functions to specialized Managed Service providers will continue to drive demand for robust and scalable security offerings.

Emerging Opportunities in Infrastructure Protection Industry

Emerging opportunities in the Infrastructure Protection Industry are abundant, driven by technological advancements and evolving global security needs. The burgeoning field of Industrial Internet of Things (IIoT) security presents a vast untapped market, requiring specialized solutions to protect connected operational technology. The growing demand for resilient and secure cloud infrastructure for critical applications offers significant growth potential. Furthermore, the increasing focus on national cybersecurity resilience and the protection of critical supply chains are creating new markets for integrated defense strategies. The development of proactive threat intelligence platforms and advanced simulation environments for testing security resilience are also key areas for innovation and market penetration.

Leading Players in the Infrastructure Protection Industry Sector

- Honeywell International Inc

- Johnson Controls International

- Lockheed Martin Corporation

- Airbus SE

- Kaspersky Lab Inc

- General Dynamics

- Rolta India Limited

- Northrop Grumman Corporation

- SCADAfence

- BAE Systems plc

- Waterfall Security Solutions

- McAfee Corp

Key Milestones in Infrastructure Protection Industry Industry

- September 2022: McAfee Corp entered a multi-year partnership with Telefonica's digital business division to enhance its cybersecurity value offer for consumers in EMEA and Latin America. This collaboration integrated McAfee's online protection solutions into Telefonica Tech's portfolio, offering more thorough device security.

- June 2022: Johnson Controls purchased Tempered Networks, a move aimed at providing globally linked buildings with zero-trust cybersecurity. This acquisition bolstered Johnson Controls' OpenBlue secure communications stack, advancing its goal of delivering inherently hack-resistant, autonomous facilities.

Strategic Outlook for Infrastructure Protection Industry Market

The strategic outlook for the Infrastructure Protection Industry market is exceptionally positive, driven by sustained geopolitical tensions, increasing cyber threats, and the continuous digitization of critical infrastructure. Future growth will be accelerated by the integration of advanced technologies like AI, machine learning, and blockchain into security frameworks. Strategic opportunities lie in the expansion of secure operational technology (OT) solutions, the development of comprehensive cybersecurity for 5G networks, and the provision of resilient cloud security for government and enterprise clients. The increasing emphasis on public-private partnerships for critical infrastructure defense will also shape market dynamics, fostering collaboration and innovation. The market is poised for significant expansion as stakeholders prioritize robust, proactive, and integrated security solutions.

Infrastructure Protection Industry Segmentation

-

1. Services

- 1.1. Risk Management Services

- 1.2. Designing, Integration, and Consultation

- 1.3. Managed Service

- 1.4. Maintenance & Support

-

2. Vertical

- 2.1. BFSI

- 2.2. Public Infrastructure &Transportation

- 2.3. Energy and Power

- 2.4. Commercial Sector

- 2.5. IT & Telecom

- 2.6. Manufacturing

- 2.7. Others

Infrastructure Protection Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Infrastructure Protection Industry Regional Market Share

Geographic Coverage of Infrastructure Protection Industry

Infrastructure Protection Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Risk Management Services

- 5.1.2. Designing, Integration, and Consultation

- 5.1.3. Managed Service

- 5.1.4. Maintenance & Support

- 5.2. Market Analysis, Insights and Forecast - by Vertical

- 5.2.1. BFSI

- 5.2.2. Public Infrastructure &Transportation

- 5.2.3. Energy and Power

- 5.2.4. Commercial Sector

- 5.2.5. IT & Telecom

- 5.2.6. Manufacturing

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Global Infrastructure Protection Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Risk Management Services

- 6.1.2. Designing, Integration, and Consultation

- 6.1.3. Managed Service

- 6.1.4. Maintenance & Support

- 6.2. Market Analysis, Insights and Forecast - by Vertical

- 6.2.1. BFSI

- 6.2.2. Public Infrastructure &Transportation

- 6.2.3. Energy and Power

- 6.2.4. Commercial Sector

- 6.2.5. IT & Telecom

- 6.2.6. Manufacturing

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. North America Infrastructure Protection Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Services

- 7.1.1. Risk Management Services

- 7.1.2. Designing, Integration, and Consultation

- 7.1.3. Managed Service

- 7.1.4. Maintenance & Support

- 7.2. Market Analysis, Insights and Forecast - by Vertical

- 7.2.1. BFSI

- 7.2.2. Public Infrastructure &Transportation

- 7.2.3. Energy and Power

- 7.2.4. Commercial Sector

- 7.2.5. IT & Telecom

- 7.2.6. Manufacturing

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Services

- 8. Europe Infrastructure Protection Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Services

- 8.1.1. Risk Management Services

- 8.1.2. Designing, Integration, and Consultation

- 8.1.3. Managed Service

- 8.1.4. Maintenance & Support

- 8.2. Market Analysis, Insights and Forecast - by Vertical

- 8.2.1. BFSI

- 8.2.2. Public Infrastructure &Transportation

- 8.2.3. Energy and Power

- 8.2.4. Commercial Sector

- 8.2.5. IT & Telecom

- 8.2.6. Manufacturing

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Services

- 9. Asia Pacific Infrastructure Protection Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Services

- 9.1.1. Risk Management Services

- 9.1.2. Designing, Integration, and Consultation

- 9.1.3. Managed Service

- 9.1.4. Maintenance & Support

- 9.2. Market Analysis, Insights and Forecast - by Vertical

- 9.2.1. BFSI

- 9.2.2. Public Infrastructure &Transportation

- 9.2.3. Energy and Power

- 9.2.4. Commercial Sector

- 9.2.5. IT & Telecom

- 9.2.6. Manufacturing

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Services

- 10. Latin America Infrastructure Protection Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Services

- 10.1.1. Risk Management Services

- 10.1.2. Designing, Integration, and Consultation

- 10.1.3. Managed Service

- 10.1.4. Maintenance & Support

- 10.2. Market Analysis, Insights and Forecast - by Vertical

- 10.2.1. BFSI

- 10.2.2. Public Infrastructure &Transportation

- 10.2.3. Energy and Power

- 10.2.4. Commercial Sector

- 10.2.5. IT & Telecom

- 10.2.6. Manufacturing

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Services

- 11. Middle East and Africa Infrastructure Protection Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Services

- 11.1.1. Risk Management Services

- 11.1.2. Designing, Integration, and Consultation

- 11.1.3. Managed Service

- 11.1.4. Maintenance & Support

- 11.2. Market Analysis, Insights and Forecast - by Vertical

- 11.2.1. BFSI

- 11.2.2. Public Infrastructure &Transportation

- 11.2.3. Energy and Power

- 11.2.4. Commercial Sector

- 11.2.5. IT & Telecom

- 11.2.6. Manufacturing

- 11.2.7. Others

- 11.1. Market Analysis, Insights and Forecast - by Services

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Honeywell International Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Johnson Controls International

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lockheed Martin Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Airbus SE

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Kaspersky Lab Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 General Dynamics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Rolta India Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Northrop Grumman Corporation*List Not Exhaustive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SCADAfence

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 BAE Systems plc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Waterfall Security Solutions

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 McAfee Corp

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Honeywell International Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Infrastructure Protection Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Infrastructure Protection Industry Revenue (billion), by Services 2025 & 2033

- Figure 3: North America Infrastructure Protection Industry Revenue Share (%), by Services 2025 & 2033

- Figure 4: North America Infrastructure Protection Industry Revenue (billion), by Vertical 2025 & 2033

- Figure 5: North America Infrastructure Protection Industry Revenue Share (%), by Vertical 2025 & 2033

- Figure 6: North America Infrastructure Protection Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Infrastructure Protection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Infrastructure Protection Industry Revenue (billion), by Services 2025 & 2033

- Figure 9: Europe Infrastructure Protection Industry Revenue Share (%), by Services 2025 & 2033

- Figure 10: Europe Infrastructure Protection Industry Revenue (billion), by Vertical 2025 & 2033

- Figure 11: Europe Infrastructure Protection Industry Revenue Share (%), by Vertical 2025 & 2033

- Figure 12: Europe Infrastructure Protection Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Infrastructure Protection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Infrastructure Protection Industry Revenue (billion), by Services 2025 & 2033

- Figure 15: Asia Pacific Infrastructure Protection Industry Revenue Share (%), by Services 2025 & 2033

- Figure 16: Asia Pacific Infrastructure Protection Industry Revenue (billion), by Vertical 2025 & 2033

- Figure 17: Asia Pacific Infrastructure Protection Industry Revenue Share (%), by Vertical 2025 & 2033

- Figure 18: Asia Pacific Infrastructure Protection Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Infrastructure Protection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Infrastructure Protection Industry Revenue (billion), by Services 2025 & 2033

- Figure 21: Latin America Infrastructure Protection Industry Revenue Share (%), by Services 2025 & 2033

- Figure 22: Latin America Infrastructure Protection Industry Revenue (billion), by Vertical 2025 & 2033

- Figure 23: Latin America Infrastructure Protection Industry Revenue Share (%), by Vertical 2025 & 2033

- Figure 24: Latin America Infrastructure Protection Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Infrastructure Protection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Infrastructure Protection Industry Revenue (billion), by Services 2025 & 2033

- Figure 27: Middle East and Africa Infrastructure Protection Industry Revenue Share (%), by Services 2025 & 2033

- Figure 28: Middle East and Africa Infrastructure Protection Industry Revenue (billion), by Vertical 2025 & 2033

- Figure 29: Middle East and Africa Infrastructure Protection Industry Revenue Share (%), by Vertical 2025 & 2033

- Figure 30: Middle East and Africa Infrastructure Protection Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Infrastructure Protection Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Infrastructure Protection Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 2: Global Infrastructure Protection Industry Revenue billion Forecast, by Vertical 2020 & 2033

- Table 3: Global Infrastructure Protection Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Infrastructure Protection Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 5: Global Infrastructure Protection Industry Revenue billion Forecast, by Vertical 2020 & 2033

- Table 6: Global Infrastructure Protection Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Infrastructure Protection Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 8: Global Infrastructure Protection Industry Revenue billion Forecast, by Vertical 2020 & 2033

- Table 9: Global Infrastructure Protection Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Infrastructure Protection Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 11: Global Infrastructure Protection Industry Revenue billion Forecast, by Vertical 2020 & 2033

- Table 12: Global Infrastructure Protection Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Infrastructure Protection Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 14: Global Infrastructure Protection Industry Revenue billion Forecast, by Vertical 2020 & 2033

- Table 15: Global Infrastructure Protection Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Infrastructure Protection Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 17: Global Infrastructure Protection Industry Revenue billion Forecast, by Vertical 2020 & 2033

- Table 18: Global Infrastructure Protection Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Infrastructure Protection Industry?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the Infrastructure Protection Industry?

Key companies in the market include Honeywell International Inc, Johnson Controls International, Lockheed Martin Corporation, Airbus SE, Kaspersky Lab Inc, General Dynamics, Rolta India Limited, Northrop Grumman Corporation*List Not Exhaustive, SCADAfence, BAE Systems plc, Waterfall Security Solutions, McAfee Corp.

3. What are the main segments of the Infrastructure Protection Industry?

The market segments include Services, Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 151.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Integration of infrastructure Protection with IoT and Cloud; Government Regulations on Infrastructure Protection.

6. What are the notable trends driving market growth?

Significant Demand in the BFSI Sector.

7. Are there any restraints impacting market growth?

Challenges Relating to Digital Transformation.

8. Can you provide examples of recent developments in the market?

In September 2022, McAfee Corp entered a multi-year partnership with Telefonica's digital business division to enhance its cybersecurity value offer for consumers in EMEA (Europe, Middle East, and Africa) and Latin America to include the online protection solutions of the American corporation into its portfolio. Telefónica Tech would incorporate the new McAfee Multi Access into its offering through this partnership arrangement to give its clients more thorough protection based on device security.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Infrastructure Protection Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Infrastructure Protection Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Infrastructure Protection Industry?

To stay informed about further developments, trends, and reports in the Infrastructure Protection Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence