Key Insights

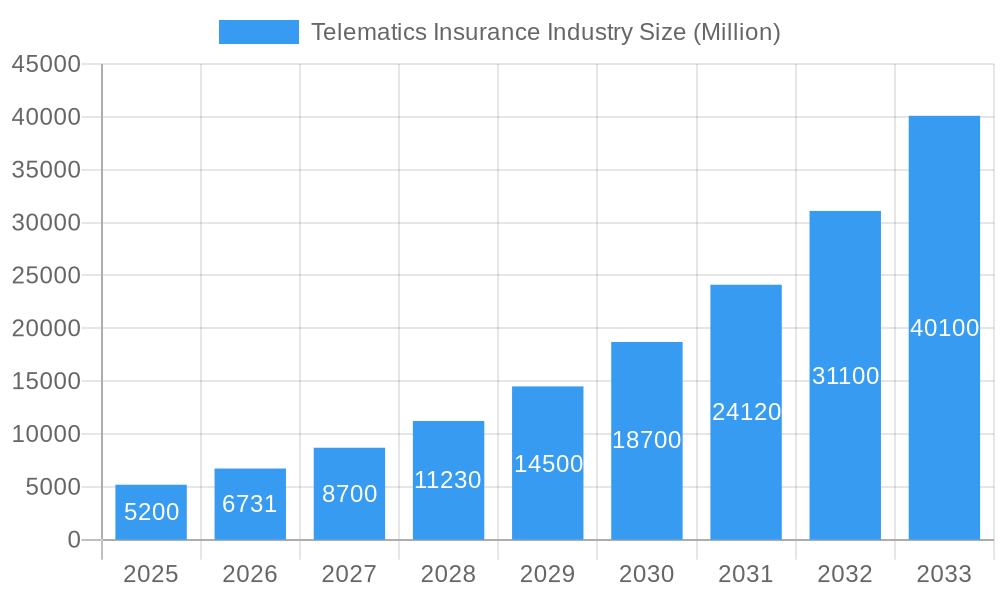

The Telematics Insurance market is projected for substantial growth, with a current market size of 5256.7 million and an anticipated Compound Annual Growth Rate (CAGR) of 21.2% through 2033. This expansion is driven by the increasing adoption of connected vehicle technology, rising consumer demand for personalized insurance, and evolving regulations promoting safer driving. Insurers are leveraging telematics data for precise risk assessment and competitive pricing, transitioning the industry towards a proactive, data-centric model. The proliferation of smartphones and in-vehicle devices further facilitates participation in Usage-Based Insurance (UBI) programs.

Telematics Insurance Industry Market Size (In Billion)

The market is segmented by usage type: Pay-as-you-drive (PAYD), Pay-how-you-drive (PHYD), and Manage-how-you-drive (MHYD). PHYD is a leading segment, offering significant savings and rewards for safe driving. Key players such as GEICO, UnipolTech, and Octo Telematics are driving innovation in data collection and analysis platforms. While data privacy concerns and initial infrastructure investment are potential restraints, the long-term benefits of reduced claims, enhanced customer loyalty, and improved road safety position telematics insurance as a future cornerstone of the automotive insurance sector.

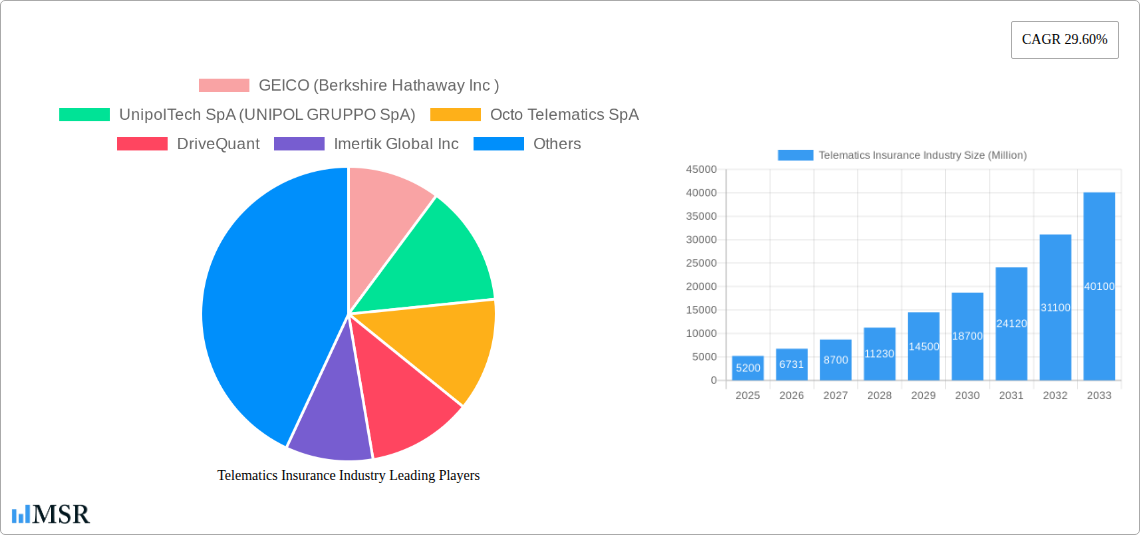

Telematics Insurance Industry Company Market Share

Explore the dynamic Telematics Insurance industry with this comprehensive report. Analyzing the period from 2019 to 2033, with 2025 as the base year, this study offers critical insights into market concentration, growth drivers, key segments, and the competitive landscape. Understand how Usage-Based Insurance (UBI), including Pay-as-you-drive, Pay-how-you-drive, and Manage-how-you-drive models, is transforming auto insurance, asset tracking, and fleet management. This report is essential for insurers, telematics providers, investors, and technology innovators targeting the expanding insurtech market.

Telematics Insurance Industry Market Concentration & Dynamics

The telematics insurance market exhibits a moderate to high concentration, with a few key players holding significant market share. GEICO (Berkshire Hathaway Inc), UnipolTech SpA (UNIPOL GRUPPO SpA), and Octo Telematics SpA are prominent entities shaping the competitive environment. Innovation ecosystems are flourishing, fueled by advancements in IoT, Artificial Intelligence (AI), and machine learning for driver behavior analysis. Regulatory frameworks are evolving globally to support data privacy and security while encouraging the adoption of UBI. Substitute products are limited, but traditional insurance models are gradually being disrupted by more data-driven approaches. End-user trends point towards increasing demand for personalized pricing and safety features. Mergers and acquisitions (M&A) activity is a significant dynamic, as seen with Targa Telematics SPA's acquisition of Earnix's telematics business, signifying a consolidation drive and expansion of digital capabilities. The market is characterized by a growing number of startups and established companies vying for dominance in the connected car insurance and fleet telematics sectors. Expected market share shifts will favor companies with robust data analytics and customer-centric offerings.

Telematics Insurance Industry Industry Insights & Trends

The telematics insurance industry is experiencing robust growth, projected to reach over 50 Million by 2025 and expand significantly by 2033. This growth is propelled by a Compound Annual Growth Rate (CAGR) of XX% during the forecast period. The primary market size for Usage-Based Insurance (UBI) is currently estimated at XX Million, with substantial contributions from both personal auto and commercial fleet sectors. Technological disruptions, including the proliferation of smart devices, in-car telematics devices, and mobile applications, are key drivers. The increasing adoption of IoT solutions in vehicles is facilitating real-time data collection on driving patterns, vehicle performance, and location. Evolving consumer behaviors, driven by a desire for personalized insurance premiums, increased safety, and cost savings, are further accelerating market penetration. Insurtech innovation is at the forefront, with companies leveraging big data analytics and AI to offer more accurate risk assessments and tailor policies to individual driving habits. The integration of telematics with other services like predictive maintenance and roadside assistance is also enhancing value propositions for consumers and businesses alike. The growing awareness of the benefits of pay-how-you-drive policies among younger demographics and accident-prone drivers is a significant trend. Furthermore, the increasing regulatory support for data-driven insurance models in various countries is creating a favorable environment for market expansion.

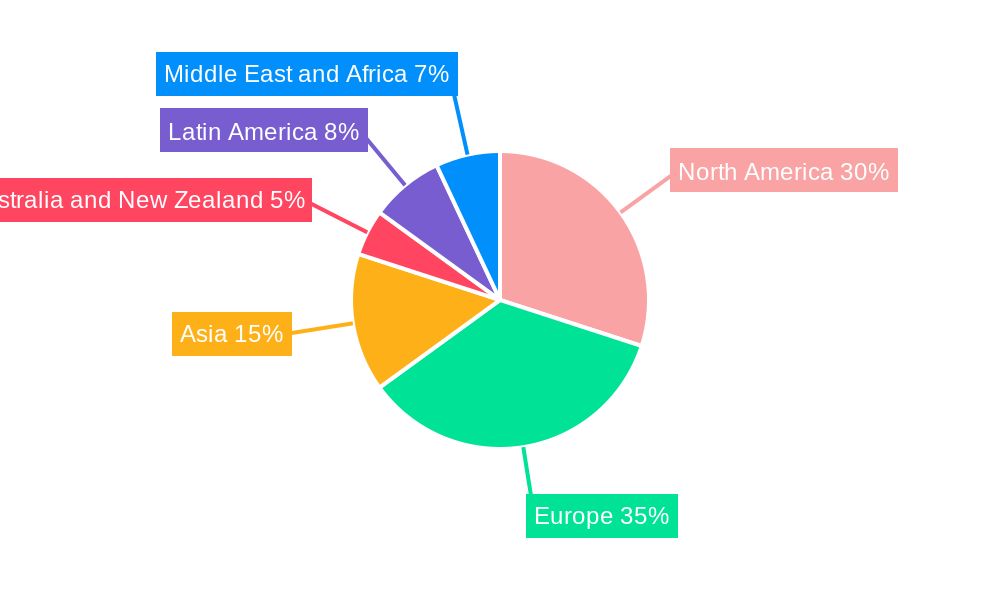

Key Markets & Segments Leading Telematics Insurance Industry

The North America region currently leads the telematics insurance industry, driven by a mature insurance market, high vehicle penetration, and a strong technological infrastructure. Within this region, the United States represents a dominant country, fueled by robust adoption of Usage-Based Insurance (UBI) programs by major insurers. Among the Usage Types, Pay-how-you-drive currently holds the largest market share, as consumers increasingly seek to demonstrate safe driving habits for reduced premiums.

- Economic Growth: Strong economic conditions in North America support higher disposable incomes, enabling consumers to invest in telematics-enabled vehicles and services.

- Infrastructure Development: Extensive road networks and a high concentration of insured vehicles provide a fertile ground for telematics deployment.

- Technological Adoption: Early and widespread adoption of smartphones and connected car technologies makes it easier for insurers to implement telematics solutions.

- Regulatory Support: Favorable regulatory environments in many US states have encouraged the development and offering of UBI policies.

The Pay-as-you-drive segment is also experiencing significant traction, particularly among low-mileage drivers and younger demographics seeking cost-effective insurance solutions. The Manage-how-you-drive segment, primarily focused on fleet management and commercial applications, is witnessing substantial growth due to its ability to optimize operational efficiency, enhance driver safety, and reduce fleet operating costs. Companies are increasingly integrating telematics for real-time fleet monitoring, route optimization, and driver performance management, contributing to the segment's dominance in the commercial sector. The European market, particularly countries like Italy and the UK, also represents a significant and growing contributor to the global telematics insurance landscape.

Telematics Insurance Industry Product Developments

The telematics insurance industry is characterized by continuous product innovation, driven by advancements in AI, machine learning, and IoT. Companies are developing sophisticated driver behavior analysis tools, offering personalized risk scores and feedback to policyholders. Applications range from enhanced road safety features and accident detection to proactive vehicle maintenance alerts. The integration of telematics with insurtech platforms is enabling seamless policy management and claims processing. The competitive edge in this market is increasingly defined by the accuracy of data collection, the intelligence of analytical insights, and the user-friendliness of the associated applications, with solutions now available for both consumer vehicles and commercial fleets.

Challenges in the Telematics Insurance Industry Market

Despite robust growth, the telematics insurance market faces several challenges. Data privacy and security concerns remain paramount, requiring robust cybersecurity measures and transparent data handling policies. Regulatory hurdles and the need for standardized data protocols across different regions can slow down adoption. The high initial cost of hardware installation for some telematics solutions can be a barrier for widespread consumer adoption. Furthermore, intense competitive pressures from both established insurance giants and agile insurtech startups necessitate continuous innovation and cost optimization, with estimated market impact on adoption rates at XX% due to these factors.

Forces Driving Telematics Insurance Industry Growth

Several key forces are propelling the telematics insurance industry forward. Technological advancements, including the increasing affordability and sophistication of telematics devices and mobile sensing technologies, are crucial enablers. Economic factors, such as rising insurance premiums and consumer demand for cost savings, are driving interest in UBI. Regulatory support and initiatives promoting safer driving practices also play a significant role. The growing awareness among consumers of the benefits of personalized insurance and enhanced vehicle safety is a powerful catalyst.

Challenges in the Telematics Insurance Industry Market

Long-term growth catalysts for the telematics insurance industry lie in continued innovation and strategic market expansions. The development of more advanced AI algorithms for predictive analytics, fraud detection, and personalized risk management will be critical. Partnerships between insurance companies, telematics providers, and automotive manufacturers are essential for deeper integration and broader reach. Exploring new markets and diversifying product offerings to include other insurance lines beyond auto, such as usage-based home or health insurance, presents significant growth potential.

Emerging Opportunities in Telematics Insurance Industry

Emerging opportunities in the telematics insurance industry are abundant. The burgeoning electric vehicle (EV) market presents a unique opportunity for telematics to monitor battery health, charging patterns, and optimize insurance policies. The integration of telematics with smart cities initiatives can lead to new data streams for urban planning and safety. The expansion of telematics into commercial insurance beyond fleets, for industries like construction and logistics, offers substantial untapped potential. Furthermore, the increasing demand for gamification and rewards-based insurance programs is creating new avenues for customer engagement and loyalty.

Leading Players in the Telematics Insurance Industry Sector

- GEICO (Berkshire Hathaway Inc)

- UnipolTech SpA (UNIPOL GRUPPO SpA)

- Octo Telematics SpA

- DriveQuant

- Imertik Global Inc

- Axa SA

- The Floow Limited

- LexisNexis Risks Solutions (Relx Group)

- Vodafone Automotive SpA (Vodafone Group PLC)

- Viasat Group

- Targa Telematics SpA

- Cambridge Mobile Telematics

- AllState Insurance Co

Key Milestones in Telematics Insurance Industry Industry

- January 2024: Targa Telematics SPA announced the acquisition of Earnix’s telematics business to expand insurance digitization. Through this acquisition, Targa assumes ownership of Drive-it, which has a solution to develop a behavioral analysis of drivers, leveraging machine learning and Artificial Intelligence technologies.

- December 2023: MiX Telematics and Powerfleet announced a business combination, which was expected to create one of the most extensive mobile asset Internet of Things (IoT) Software-as-a-Service (SaaS) providers in the world.

Strategic Outlook for Telematics Insurance Industry Market

The strategic outlook for the telematics insurance industry is exceptionally positive, driven by ongoing technological advancements and evolving consumer expectations. Growth accelerators include the further integration of AI and machine learning for enhanced risk assessment and personalized customer experiences. Strategic opportunities lie in expanding into new geographic markets and diversifying product portfolios to cater to emerging vehicle technologies like EVs. The ongoing consolidation within the industry, marked by key M&A activities, will likely lead to stronger, more innovative players. Focus on data analytics, cybersecurity, and user-centric design will be paramount for sustained success and capturing future market potential, estimated to grow by XX% in the coming years.

Telematics Insurance Industry Segmentation

-

1. Usage Type

- 1.1. Pay-as-you-drive

- 1.2. Pay-how-you-drive

- 1.3. Manage-how-you-drive

Telematics Insurance Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Telematics Insurance Industry Regional Market Share

Geographic Coverage of Telematics Insurance Industry

Telematics Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Usage Type

- 5.1.1. Pay-as-you-drive

- 5.1.2. Pay-how-you-drive

- 5.1.3. Manage-how-you-drive

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia

- 5.2.4. Australia and New Zealand

- 5.2.5. Latin America

- 5.2.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Usage Type

- 6. Global Telematics Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Usage Type

- 6.1.1. Pay-as-you-drive

- 6.1.2. Pay-how-you-drive

- 6.1.3. Manage-how-you-drive

- 6.1. Market Analysis, Insights and Forecast - by Usage Type

- 7. North America Telematics Insurance Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Usage Type

- 7.1.1. Pay-as-you-drive

- 7.1.2. Pay-how-you-drive

- 7.1.3. Manage-how-you-drive

- 7.1. Market Analysis, Insights and Forecast - by Usage Type

- 8. Europe Telematics Insurance Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Usage Type

- 8.1.1. Pay-as-you-drive

- 8.1.2. Pay-how-you-drive

- 8.1.3. Manage-how-you-drive

- 8.1. Market Analysis, Insights and Forecast - by Usage Type

- 9. Asia Telematics Insurance Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Usage Type

- 9.1.1. Pay-as-you-drive

- 9.1.2. Pay-how-you-drive

- 9.1.3. Manage-how-you-drive

- 9.1. Market Analysis, Insights and Forecast - by Usage Type

- 10. Australia and New Zealand Telematics Insurance Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Usage Type

- 10.1.1. Pay-as-you-drive

- 10.1.2. Pay-how-you-drive

- 10.1.3. Manage-how-you-drive

- 10.1. Market Analysis, Insights and Forecast - by Usage Type

- 11. Latin America Telematics Insurance Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Usage Type

- 11.1.1. Pay-as-you-drive

- 11.1.2. Pay-how-you-drive

- 11.1.3. Manage-how-you-drive

- 11.1. Market Analysis, Insights and Forecast - by Usage Type

- 12. Middle East and Africa Telematics Insurance Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Usage Type

- 12.1.1. Pay-as-you-drive

- 12.1.2. Pay-how-you-drive

- 12.1.3. Manage-how-you-drive

- 12.1. Market Analysis, Insights and Forecast - by Usage Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 GEICO (Berkshire Hathaway Inc )

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 UnipolTech SpA (UNIPOL GRUPPO SpA)

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Octo Telematics SpA

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 DriveQuant

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Imertik Global Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Axa SA

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 The Floow Limited

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 LexisNexis Risks Solutions (Relx Group)

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Vodafone Automotive SpA (Vodafone Group PLC)

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Viasat Group

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Targa Telematics SpA

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Cambridge Mobile Telematics

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 AllState Insurance Co

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.1 GEICO (Berkshire Hathaway Inc )

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Telematics Insurance Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Telematics Insurance Industry Revenue (million), by Usage Type 2025 & 2033

- Figure 3: North America Telematics Insurance Industry Revenue Share (%), by Usage Type 2025 & 2033

- Figure 4: North America Telematics Insurance Industry Revenue (million), by Country 2025 & 2033

- Figure 5: North America Telematics Insurance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Telematics Insurance Industry Revenue (million), by Usage Type 2025 & 2033

- Figure 7: Europe Telematics Insurance Industry Revenue Share (%), by Usage Type 2025 & 2033

- Figure 8: Europe Telematics Insurance Industry Revenue (million), by Country 2025 & 2033

- Figure 9: Europe Telematics Insurance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Telematics Insurance Industry Revenue (million), by Usage Type 2025 & 2033

- Figure 11: Asia Telematics Insurance Industry Revenue Share (%), by Usage Type 2025 & 2033

- Figure 12: Asia Telematics Insurance Industry Revenue (million), by Country 2025 & 2033

- Figure 13: Asia Telematics Insurance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Australia and New Zealand Telematics Insurance Industry Revenue (million), by Usage Type 2025 & 2033

- Figure 15: Australia and New Zealand Telematics Insurance Industry Revenue Share (%), by Usage Type 2025 & 2033

- Figure 16: Australia and New Zealand Telematics Insurance Industry Revenue (million), by Country 2025 & 2033

- Figure 17: Australia and New Zealand Telematics Insurance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Latin America Telematics Insurance Industry Revenue (million), by Usage Type 2025 & 2033

- Figure 19: Latin America Telematics Insurance Industry Revenue Share (%), by Usage Type 2025 & 2033

- Figure 20: Latin America Telematics Insurance Industry Revenue (million), by Country 2025 & 2033

- Figure 21: Latin America Telematics Insurance Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Middle East and Africa Telematics Insurance Industry Revenue (million), by Usage Type 2025 & 2033

- Figure 23: Middle East and Africa Telematics Insurance Industry Revenue Share (%), by Usage Type 2025 & 2033

- Figure 24: Middle East and Africa Telematics Insurance Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Telematics Insurance Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 2: Global Telematics Insurance Industry Revenue million Forecast, by Region 2020 & 2033

- Table 3: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 4: Global Telematics Insurance Industry Revenue million Forecast, by Country 2020 & 2033

- Table 5: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 6: Global Telematics Insurance Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 8: Global Telematics Insurance Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 10: Global Telematics Insurance Industry Revenue million Forecast, by Country 2020 & 2033

- Table 11: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 12: Global Telematics Insurance Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: Global Telematics Insurance Industry Revenue million Forecast, by Usage Type 2020 & 2033

- Table 14: Global Telematics Insurance Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Telematics Insurance Industry?

The projected CAGR is approximately 21.2%.

2. Which companies are prominent players in the Telematics Insurance Industry?

Key companies in the market include GEICO (Berkshire Hathaway Inc ), UnipolTech SpA (UNIPOL GRUPPO SpA), Octo Telematics SpA, DriveQuant, Imertik Global Inc, Axa SA, The Floow Limited, LexisNexis Risks Solutions (Relx Group), Vodafone Automotive SpA (Vodafone Group PLC), Viasat Group, Targa Telematics SpA, Cambridge Mobile Telematics, AllState Insurance Co.

3. What are the main segments of the Telematics Insurance Industry?

The market segments include Usage Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5256.7 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Usage-Based Insurance by Insurance Companies; Increase in Innovation in the Automotive Industry Drive the Market Growth.

6. What are the notable trends driving market growth?

Pay-How-You-Drive Segment to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Increasing Adoption of Usage-Based Insurance by Insurance Companies; Increase in Innovation in the Automotive Industry Drive the Market Growth.

8. Can you provide examples of recent developments in the market?

In January 2024, Targa Telematics SPA announced the acquisition of Earnix’s telematics business to expand insurance digitization. Through this acquisition, Targa assumes ownership of Drive-it, which has a solution to develop a behavioral analysis of drivers, leveraging machine learning and Artificial Intelligence technologies.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Telematics Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Telematics Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Telematics Insurance Industry?

To stay informed about further developments, trends, and reports in the Telematics Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence